Eva and her husband Patrick live in Central Oregon where they both work as nurses. Their two children are now grown and Eva and Patrick are nearing traditional retirement age. Eva is concerned they may be behind on their retirement savings and would like our help analyzing their assets. A major concern for the couple is a family history of Alzheimer’s on Patrick’s side. Eva would like him to be able to retire sooner rather than later so that he’s able to enjoy retirement for as long as possible. Let’s dig in to help Eva and Patrick map out their retirement!

What’s a Reader Case Study?

Case Studies address financial and life dilemmas that readers of Frugalwoods send in requesting advice. Then, we (that’d be me and YOU, dear reader) read through their situation and provide advice, encouragement, insight and feedback in the comment section.

For an example, check out the last case study. Case Studies are updated by participants (at the end of the post) several months after the Case is featured. Visit this page for links to all updated Case Studies.

The Goal Of Reader Case Studies

Reader Case Studies intend to highlight a diverse range of financial situations, ages, ethnicities, locations, goals, careers, incomes, family compositions and more!

The Case Study series began in 2016 and, to date, there’ve been 69 Case Studies. I’ve featured folks with annual incomes ranging from $17k to $200k+ and net worths ranging from -$300k to $2.9M+.

I’ve featured single, married, partnered, divorced, child-filled and child-free households. I’ve featured gay, straight and trans people. I’ve featured men, women and non-binary folks. I’ve had cat people and dog people. I’ve featured folks from the US, Australia, Canada, England, South Africa, Spain, Finland and France.

I’ve featured people with PhDs and people with high school diplomas. I’ve featured people in their early 20’s and people in their late 60’s. I’ve featured folks who live on farms and folks who live in New York City.

The goal is diversity and only YOU can help me achieve that by emailing me your story! If you haven’t seen your circumstances reflected in a Case Study, I encourage you to apply to be a Case Study participant by emailing mrs@frugalwoods.com.

Reader Case Study Guidelines

I probably don’t need to say the following because you folks are the kindest, most polite commenters on the internet, but please note that Frugalwoods is a judgement-free zone where we endeavor to help one another, not condemn.

There’s no room for rudeness here. The goal is to create a supportive environment where we all acknowledge we’re human, we’re flawed, but we choose to be here together, workshopping our money and our lives with positive, proactive suggestions and ideas.

A disclaimer that I am not a trained financial professional and I encourage people not to make serious financial decisions based solely on what one person on the internet advises.

I encourage everyone to do their own research to determine the best course of action for their finances. I am not a financial advisor and I am not your financial advisor.

With that I’ll let Eva, today’s Case Study subject, take it from here!

Eva’s Story

Hello Frugalwoods Friends! I’m Eva and I’m 56. My husband Patrick, also 56, and I have two adult children, three cats, and a fresh water tank full of fish. We live in Central Oregon where we both work as RNs. Patrick has a side gig as a medical death investigator, which might have been his primary occupation if it were more lucrative.

We’ve been married for 28 years and have lived in Central Oregon for 20 of those years. We love the area, although not the increase in population. Our son is 23, living on his own, and is nearly finished with his associate’s degree. Our daughter is 20 and is in her 3rd year (of 8!) at a university 2.5 hrs away. She recently started renting, but had previously been in student housing, spending all breaks at home. The fur and fin portion of our family consists of three spoiled cats and 15 colorful fish. Patrick’s mother (his father is deceased) and my parents also moved to Central Oregon in the last 8 years, and we are thankful to have them close by.

Eva’s Career

I work on a Med-Surg/postop unit. Through the pandemic, surgeries have been drastically reduced. Instead, mostly very sick patients struggling with acute and chronic illnesses and trauma surgery patients make up the bulk of my unit. I’ve taken care of only a few Covid patients and definitely count myself very fortunate. Our hospital has grappled with staffing shortages, units filled to capacity, and nurse burnout in the harder hit units. I commend all of the emergency and ICU nurses, physicians and ancillary staff who have been caring for those very sick patients for months on end!

Patrick’s Career

Patrick is more on the Covid-testing side, having swabbed hundreds of people and vaccinated many as well. In addition, he is a medical death investigator. He goes to scenes (car accidents, exposure deaths, falls from a height, suicides, deaths in homes, and a few in the hospital). He does not go to Covid deaths, but does wear PPE at scenes where the possibility of exposure is unknown. He is paid a flat rate per 24 hrs on-call, a per case rate for decedents who go for autopsy, and also mileage. While I have accompanied him to scenes a few times and joined him at funeral homes when postmortem fluids are needed, this is not a form of nursing that calls to me.

The Lives of Two Nurses

Nursing is a stressful vocation and sometimes hard to turn off after the shift is complete. We consider it a privilege to be able to help when people are feeling their most vulnerable. It’s rewarding to see someone come through a challenging medical event. We’re happy to have chosen our careers and also very thankful to have saved money during the pandemic when so many have struggled financially and/or lost their livelihoods.

Patrick and Eva’s Hobbies

When we’re not working, we enjoy kayaking on nearby lakes, cross-country skiing in the nearby mountains, hiking to waterfalls around Oregon, motorcycle rides to coffee shops and gardening. I’m more of an introvert while Patrick is an extrovert, but we’ve made it work. I enjoy reading, baking, yoga, rollerskating, drinking coffee and the occasional White Russian! Patrick enjoys riding ALL of his motorcycles (the deal is he can have 1 motorcycle for every cat I adopt), drumming with his band, fishing, playing disc golf, DIYing around the house, and SO much more…

What feels most pressing right now? What brings you to submit a Case Study?

I’m concerned we’re a bit behind on retirement savings, but, I would like Patrick to retire sooner rather than later. He has a strong family history of Alzheimer’s disease, and is very concerned this will be his legacy as well. His father and grandfather both died from this in their early 70s. They led less-healthy lifestyles, so we’re hoping the odds are in Patrick’s favor.

As of now he hasn’t experienced any difficulties, but because this is a possibility, I would like him to retire from nursing at age 62 (which is 5.5 years from now) to allow more time for his hobbies. The plan is for me to continue working until I’m 65 to grow our savings and cover our health benefits. I have no idea if these timeframes are feasible with our current savings/spending rates.

Patrick listens attentively when I discuss saving more, reducing spending, and planning ahead, but he is also of the mindset that he doesn’t want to do without now when there’s a possibility that he won’t be able to enjoy it later.

I feel overwhelmed when reading about diversified portfolios, taxes, and enough vs. too much insurance. I’m not very tech-savvy, so I have a difficult time finding the information I need regarding our accounts, i.e., fees we’re paying, how and where to transfer funds. As a result, I don’t touch anything and just let it ride. I have no idea how to invest (choosing funds if we do open an IRA — or if it’s too late to see much growth).

Kids’ College

Because we didn’t start 529 accounts for our children, we’re helping our daughter pay as she goes to offset the amount she needs to obtain in loans. Our deal (for both kids) is that we’ll give them $50,000 over 4 years and then they’re responsible for the rest. Thankfully our daughter is a good saver and has worked throughout college, especially during school breaks. I understand the “put your own oxygen mask on first” approach, but I feel like we owe it to our children to help launch them with the least amount of debt possible. Our son chose a community college, is working, and as of now does not want to go further. If this changes, we would want to help him with any additional education.

We have discussed moving to a low cost of living (LCOL) area after retirement. Our current home is two levels, and it makes sense to look for a smaller single-level home. Central Oregon is a very desirable location, so I don’t think we’ll have much trouble selling our home. But, where to go? We LOVE snow, mountains, and lakes. Do we even consider a move if my husband may have health issues in the next decade or so? Our friends and family are here, at least for now. Seems like this may be a wait and see how things play out situation.

What’s the best part of your current lifestyle/routine?

We love our home and quiet neighborhood, four seasons, our short commute to work/amenities, all the beautiful nature that makes up Oregon, and of course, having family close by. When we’re home, we are relaxed and calm. We enjoy cooking, especially with veggies and fruits from our garden. There’s a brewery that makes great appetizers within walking distance and has outdoor seating year-round (outdoor heaters!).

There’s a river that runs through our town, in addition to lots of parks for leisurely walks and picnics. This sounds silly as a consideration, but our town also has a Costco, which we take advantage of twice a month for staples and good deals on cat litter.

What’s the worst part of your current lifestyle/routine?

When we moved to our town, the population was 50,000. This has more than doubled in the last 20 years. The surrounding streets and roadways were not built to handle this much growth, and our city government has struggled to keep up with maintenance and increased traffic. It’s not unheard of to sit at a traffic light through three cycles during peak times before it’s your turn. Thankfully, our commutes are off-peak. There are larger cities, about three hours from us, where crime has increased exponentially and we are concerned it is creeping our way.

Eva and Patrick’s Retirement Budget

I went ahead and figured out our anticipated Social Security income:

Eva:

- age 65: $1,853 per month

- age 67: $2,217 per month

- age 70: $2,887 per month

Patrick:

- age 65: $2,583 per month

- age 67: $3,014 per month

- age 70: $3,797 per month

Patrick’s benefit at age 62 is $2,058, but we don’t plan on taking his benefit until age 65. I would also like to hold off until age 67 to take my benefit, but am unsure how our finances will look to gauge whether this would be feasible. I have read that SS is in dire straits and our benefit could be reduced by 30%.

I also made this rough estimate of our expenses in retirement, not knowing how much costs will increase over the next 9 years:

| Item | Amount | Notes |

| Medical/Rx/dental | $800 | I have no idea how much Medicare costs, and don’t think it covers dental? |

| Fun/travel | $750 | Travel in the US |

| Food | $600 | |

| House (taxes and insurance) | $500 | smaller house in lower COL town? |

| Insurance/maint. (car/MC) | $300 | |

| Gas/Electric | $250 | |

| Long-term care insurance | $240 | A big guess, maybe reasonable if it’s acquired now as opposed to at age 62? |

| House maintenance | $200 | |

| Restaurants | $200 | |

| Clothing/shoes/personal | $200 | |

| Fuel | $150 | Would like a new-to-us car in 9 yrs…hybrid? EV? |

| Water | $150 | |

| Cats (2) | $150 | |

| Internet/Netflix/Hulu | $130 | Currently we don’t pay for Hulu–we use our daughter’s account |

| Misc. (toiletries, etc.) | $100 | |

| Cell phones | $100 | perhaps less with an MVNO? |

| Gifts | $100 | |

| Donations | 50 | also plan to continue volunteering |

| Trash | $40 | |

| National Parks pass | $15 | |

| TOTAL: | $5,025 |

Realistically, I think we’ll be spending at least $5,500 month/$66,000 year.

Where Eva and Patrick Want to be in 10 years:

- Finances: We would like to be retired with enough saved to sustain us without worrying that our children might need to help us at any point. “Enough” sounds so vague.

- Lifestyle: Living in a smaller, LCOL town, possibly in Montana? We’re hoping our kids will stay somewhere in the PNW, so that we’re within a day’s travel from them.

- We have one big bucket list item: a trip to Ireland either prior to retirement or right at the beginning of retirement that we’ve been talking about taking. Then, smaller trips around the US during retirement.

- Perhaps we could spend the first year of retirement looking for our last home? Having water close by for kayaking and fishing close by for Patrick would be ideal. Continuing our current outdoor hobbies with more time to pursue them as our health allows. We’ve both spent time volunteering, and would enjoy continuing to give back in that way to our community.

- Career: If needed, very part-time work would be okay in both our minds, perhaps 15 hours a week. Patrick plans to continue being a medical death investigator until age 65. After that, getting those calls in the middle of the night will probably be too much.

Eva and Patrick’s Finances

Income

| Item | Amount | Notes |

| Patrick’s net income per month | $4,211 | P’s net salary, minus medical, dental, vision insurance for family, 403b (24%) contributions, and taxes |

| Eva’s net income per month | $3,337 | My net salary, minus 403b (29%) contributions, union dues, and taxes. |

| Patrick’s net income side hustle per month | $900 | This varies monthly, so this is the average. No deductions – we pay estimated quarterly taxes |

| Monthly subtotal: | $8,448.00 | Based on 26 paychecks annually |

| Annual total: | $108,898.00 | Based on 26 paychecks annually |

Mortgage Details

Our home is paid off! We purchased it for $206k in 2002 and Zillow now says it’s worth $619k.

Debts: $0

Assets

| Item | Amount | Notes | Interest/type of securities held/Stock ticker | Name of bank/brokerage | Expense Ratio |

| Eva’s 403b | $126,175 | Current employer | Mix of stocks and bonds “2030 fund” | Fidelity | No idea |

| Patrick’s 403b | $121,258 | Current employer | Mix of stocks and bonds “2030 fund” | Fidelity | No idea |

| Savings | $90,000 | Emergency fund.

I put $2,000 into savings every month, without fail. |

Negligible | US Bank | No fees |

| Eva’s rollover 403b | $55,214 | Previous employer | Mix of stocks and bonds “2030 fund” | Fidelity | No idea |

| Eva’s 403b | $11,728 | Previous employer | Mix of stocks and bonds, I really have no idea. | Lincoln | No idea |

| Individual stock | $7,840 | Costco | |||

| Checking account | $3,500 | Monthly bills | Negligible | US Bank | No fees |

| US savings bonds | $2,267 | Maturing in next 2-4 years | |||

| SEP IRA | $1,020 | Opened this thinking we could deduct it and lower our AGI (apparently not if we already contribute to 403b) | 50/50 mix stocks and bonds, randomly chosen | ||

| Total: | $419,002 |

Vehicles

| Vehicle make, model, year | Valued at | Mileage | Paid off? |

| Toyota 4Runner, 2016 | $33,000. These values are crazy, nearly what we originally paid. | 59,800 | Yes |

| Toyota 86, 2017 | $26,000. The used car market is unbelievable right now! | 9,755 (yes, this low) | Yes |

| BMW 1000R, 2020 | $17,650 | 13,400 | Yes |

| Honda XR, 2015 | $4,800 | 4,300 | Yes |

| Honda Shadow, 2001 | $2,700 | 36,300 | Yes |

| Total: | $84,150.00 |

Expenses

| Item | Amount | Notes |

| Daughter’s college tuition | $1,042 | Wish we had started a 529 years ago. This ends in June 2023. |

| Grocery store/Costco | $619 | Includes household supplies (TP, toothpaste, cat food, laundry soap, etc). Our daughter was at home for 4 months in this average. |

| Insurance (cars, motorcycles, kids’ cars, life) | $505 | 4 vehicles – daughter in college, son pays his college tuition and we pay his insurance – ends in 2/2022. 3 motorcycles. Term life insurance for both of us – ends when Patrick turns 62 & daughter graduates (State Farm). This should reduce quite a bit in retirement… 1 car, 1 motorcycle and no life insurance. |

| Quarterly tax payments | $500 | Side hustle, in addition to no deductions. When Patrick retires from nursing, we’ll be in a much lower tax bracket. |

| Property Taxes paid annually for small discount | $298 | |

| Home improvements | $292 | Xeriscaped front yard this year, planning a new fence next year, roof the year after that, other home maintenance |

| Restaurants | $210 | The cost of dining out keeps getting more and more $$. |

| Vacation | $167 | |

| Cell service for 4 (Verizon) | $155 | We continue to pay this for kids as well. Patrick requires 100% reliability for side gig. This is unlimited data. This should be cut in half by retirement, maybe even less if we can go with an MVNO. |

| Gifts | $148 | Christmas is a big part of this number. |

| Fuel for vehicles | $145 | Includes 2 weeks of solo MC vacations for Patrick annually. |

| Water | $116 | May decrease after recent xeriscaping front yard |

| Entertainment | $90 | |

| Internet | $85 | Upgraded to best package when our daughter came home for online college in 3/2020 and we never reduced it back. |

| Cats/fish tank (litter, vet, fish food, filters) | $76 | One cat gets a dental cleaning each year. |

| Electricity | $71 | Mostly A/C in the summer. |

| Alcohol | $62 | |

| Home insurance paid annually | $59 | State Farm |

| Gas | $53 | |

| Clothing/shoes | $52 | Includes annual scrubs for work. |

| Vehicle/MC maintenance/registrations | $41 | Oil changes, air filters. Should decrease quite a bit in retirement. |

| Annual 2 cords firewood (wood stove) | $37 | This supplements our heat from October to March |

| Medical/Dental copays/uncovered | $36 | Mostly lab work |

| Subscriptions | $31 | Netflix, Amazon Prime, Hallmark |

| Personal care (haircuts, color) | $31 | Patrick colors my hair for me every 3 months. |

| Medical prescriptions | $25 | |

| Trash/Recycling/Yard debris | $22 | |

| Household repairs/maintenance | $19 | Toilet flapper, air filters, things that break. |

| Charitable donations | $17 | We also volunteer at the food pantry 9 hours/month |

| RN license renewal x2 | $13 | Every other year. This will be gone in retirement. |

| Starbucks | $10 | Majority of this is during the holidays. |

| Annual national/local parks passes | $10 | |

| Monthly subtotal: | $5,037.00 | |

| Annual total: | $60,444.00 |

Credit Card Strategy

| Card Name | Rewards Type? | Bank/card company |

| Citicard* | Cash rewards | |

| Discover | Cash rewards | |

| Target | 5% off purchases | |

| Kohl’s | Only used in combination with 30% off coupon 3-4 x year. |

*affiliate link

Eva’s Questions for You:

- If we rein in our spending, does it look feasible for Patrick to retire at 62? If he doesn’t take SS benefits until 65, what happens during those three years? The benefit amount stays stagnant? Decreases from current estimates?

-

One of Eva & Patrick’s cats Since we’re getting older, is it too late to funnel money that has been accumulating in our emergency fund into ETFs instead? Or, would opening IRAs be a better idea, funding them with some of the money in our EF currently? Is there a rule against continuing to add money to the IRA from my previous employer?

- We’re putting quite a bit into our 403b’s annually (approx. $24,000 for me and $25,000 for Patrick), but not the max. Should we max these before considering opening or adding to any other accounts?

- Watching families at the hospital struggle with where to place a grandparent who has been living independently, and suddenly can no longer live independently, has me wondering if we should be looking into long-term care insurance now while we’re young enough to qualify for a lower premium? I originally thought we would do this when our term life insurance ended in 6/2027 (replace one bill with another).

- What, if anything, should we do with the Sofi account we opened?

- Our US savings bonds are nearing maturity. It’s not a substantial sum, but is there anything we can do with that money to ease our tax burden? Should they be redeemed as soon as they mature? Could they be used to pay our daughter’s tuition (again to reduce tax on gains)?

- How do we ensure the security of our personal information online? I really want to track spending, especially as a method for Patrick and I to realize our wasteful spending, but am very wary of using Personal Capital (or any software tool like this) because of the potential for hacking…all our account info in one location, YIKES!

Liz Frugalwoods’ Recommendations

Eva and Patrick are doing incredibly well! I appreciate the thoughtful mapping of their retirement and think they’ll be pleasantly surprised to hear they’re in great shape. I’m grateful to Eva and Patrick for dedicating their lives to helping others and want to thank them for these lifetimes of service. Now, let’s hop right onto Eva’s questions!

Eva’s Question #1: If we rein in our spending, does it look feasible for Patrick to retire at 62?

I will not leave you hanging: YES.

To help Eva and Patrick visualize their retirement, here’s a chart outlining their upcoming years of partial and full retirements and their respective Social Security-taking years. I will email this chart to Eva so that she and Patrick can change any of the variables they’d like.

Income

| Income | Amount |

| Eva’s Current Income | $3,337 |

| Patrick’s Current Income | $4,211 |

| Patrick’s Side Hustle Income | $900 |

| Eva’s projected Social Security at age 67 | $2,217 |

| Patrick’s projected Social Security at age 65 | $2,583 |

Breakdown by Year

| Year | Eva’s Net Income (Annual) | Patrick’s Net Income (Annual) | Expenses (Annual) | Net (income minus expenses) | Notes | Patrick & Eva’s Age (this is easy because they’re the same age!) |

| 2022 | $40,044 | $61,332 | $60,444 | $40,932 | 57 | |

| 2023 | $40,044 | $61,332 | $60,444 | $40,932 | 58 | |

| 2024 | $40,044 | $61,332 | $60,444 | $40,932 | 59 | |

| 2025 | $40,044 | $61,332 | $60,444 | $40,932 | 60 | |

| 2026 | $40,044 | $61,332 | $60,444 | $40,932 | Patrick retires from full-time nursing at the end of this calendar year; continues death investigation side hustle | 61 |

| 2027 | $40,044 | $10,800 | $60,444 | -$9,600 | This reflects Patrick’s income from the death investigation side hustle; does not include taking any Social Security | 62 |

| 2028 | $40,044 | $10,800 | $60,444 | -$9,600 | 63 | |

| 2029 | $40,044 | $10,800 | $60,444 | -$9,600 | 64 | |

| 2030 | $40,044 | $10,800 | $60,444 | -$9,600 | Eva retires at the end of this calendar year; Patrick retires from his side hustle at the end of the calendar year as well | 65 |

| 2031 | $0 | $30,996 | $66,000 | -$35,004 | Patrick starts taking Social Security at the start of this calendar year | 66 |

| 2032 | $0 | $30,996 | $66,000 | -$35,004 | 67 | |

| 2033 | $26,604 | $30,996 | $66,000 | -$8,400 | Eva starts taking Social Security at the start of this calendar year | 68 |

| 2034 | $26,604 | $30,996 | $66,000 | -$8,400 | 69 | |

| 2035 | $26,604 | $30,996 | $66,000 | -$8,400 | The difference between their planned spending and their Social Security will be roughly $8,400 per year. | 70 |

I find it really helpful to see a breakdown year by year to understand what’s going to happen with all the variables in their plan. As we can see, when it all settles out and they’re both fully retired and both taking Social Security (starting in 2033), I project they’ll have a shortfall of about $8,400 annually (that’s the difference between their projected spending and their anticipated Social Security payments). But this is not a problem because they have retirement savings in addition to Social Security. Way to go, Eva and Patrick! Let’s take a look at those investments now:

Eva and Patrick’s Retirement Investments

| Item | Amount |

| Eva’s 403b | $126,175 |

| Patrick’s 403b | $121,258 |

| Eva’s rollover 403b | $55,214 |

| Eva’s old 403b | $11,728 |

| Sep IRA | $1,020 |

| TOTAL: | $315,395 |

If Eva and Patrick took a 3.5% annual rate of withdrawal from their overall retirement assets today, they’d have $11,038 annually. This is fantastic because:

- They shouldn’t need to withdraw anything from these accounts until 2027 when Patrick retires from full-time nursing.

- They’re still working and still saving into these accounts, which means they’ll continue to grow.

- According to their projections–and my chart above–they’ll only need circa $8,400 annually to make up the difference between Social Security and their expenses.

- Additionally, Required Minimum Distributions (RMDs) will kick in for these accounts when they turn 72. I’ll address those specifics in a moment.

This means that, according to all of these calculations, Eva and Patrick are set up for a smooth, fully-funded retirement, assuming they continue to save and invest at their current rate for the remainder of their working years. This doesn’t even take into account their massive amount of cash–over $95k–IN ADDITION TO their paid-off house. Eva and Patrick, you’re in a position many folks would envy. Far from being “behind” on retirement, I’d say you’re ahead!

Eva’s Question #2: Since we’re getting older, is it too late to funnel money that has been accumulating in our emergency fund into ETFs instead?

Eva’s correct that they have a pretty large emergency fund at this point: $95k plus a paid-off house.

- On one hand, it’s nice to have this much of a cash cushion. Who doesn’t like cash?

- On the other hand, there’s a large opporunity cost to not investing this money.

Looked at from one angle, Patrick and Eva are nearing retirement. Looked at from another angle, they’re only 56 and are both active and healthy–their lifespans could be another 40+ years!

There’s a lot to weigh in deciding what to do with this money and it boils down to their risk tolerance. The safest, least-risky thing to do is to keep this money in cash. The most aggressive potential for higher returns (and higher loses) would be to invest all of it. I imagine a middle ground between the two will feel most comfortable. I’ll outline some options in a minute.

To chime into Eva’s third question, I don’t think there’d be anything wrong with fully maxing out their 403bs for their remaining working years.

That being said, we established above that their retirement is already in great shape. However, more money invested for retirement could mean a larger retirement spending budget and more travel, more hobbies, etc. Plus, it’s not like they need to save more cash and so investing more into retirement would be great. If it sounds like I’m not really answering this question, it’s because I’m not. There’s not really a right or wrong answer here, just different options that’ll fluctuate based on: their risk tolerance, their projected longevity, and their overall tax picture.

The first order of business with this $95k is for Patrick and Eva to determine how much they feel comfortable keeping in cash as an emergency fund. If they go by the six-month-of-expenses rule, that’d be $30,222 to keep in cash as an emergency fund. In that scenario, they’d have $64,778 leftover.

Here are some options for that leftover $65k:

1) Open a taxable investment account with a brokerage, such as Fidelity or Vanguard.

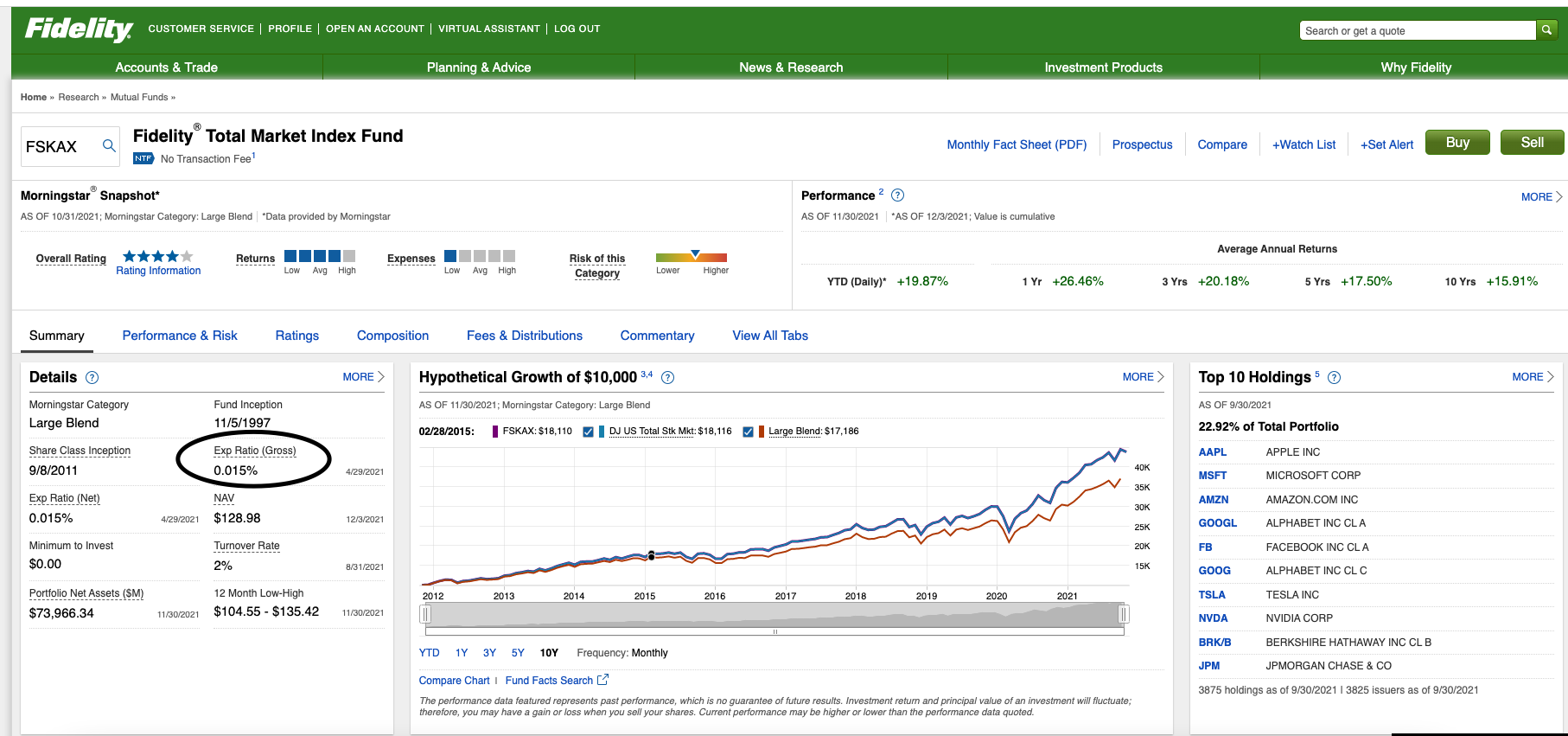

For my own personal taxable investment account, I’ve selected low-fee, total-market index funds. Understanding the fees–also called “expense ratios”–on these funds is critical. Eva noted she’s unsure how to determine these fees, so I’ll do a little tutorial. I will tell you that I personally was SO confused about this until I finally sat down, read through my fund worksheets and realized, “Oh! it’s just a little percentage right there! Voila!”

Tutorial Sidenote: How to Find a Fund’s Expense Ratio

Eva, we’re going to use one of my investment funds as an example today.

I first log into my account on Fidelity.com, then I click on “Taxable Investment” and then “Positions.” Now I’m on a screen where I can see my “Symbols,” which are the acronyms for the funds I own. Today we’re going to look at my FSKAX, which is Fidelity’s Total Market Index Fund. I click on “FSKAX,” then select “research” and “research” again, which brings me to this screen, which is an overview of the fund.

To be honest, it’s actually probably easier to just google the fund in question…. either way, here’s what you’re looking at.

I took the liberty of circling “Exp Ratio (Gross),” which as you can see is 0.015%. What this means is that this Index Fund, FSKAX, offered by the brokerage firm Fidelity, has an Expense Ratio–also known as a fee–of 0.015%. Ok but what does that actually mean?!

According to Forbes:

An expense ratio is an annual fee charged to investors who own mutual funds and exchange-traded funds (ETFs). High expense ratios can drastically reduce your potential returns over the long term, making it imperative for long-term investors to select mutual funds and ETFs with reasonable expense ratios (source)

Forbes goes on to explain how these fees are calculated:

Expense ratios are calculated with the following equation:

Total Fund Expenses / Total Fund Assets Under Management = Expense Ratio

For example, if it costs $1 million to run a fund in a given year and that fund held $100 million in assets, its expense ratio would be 1%.

Ok now I feel like I’m just quoting this entire Forbes article, but, they do a really good job explaining this! So, here’s more from Forbes:

Over time, expense ratios can have a significant impact on your returns from mutual funds and ETFs.

While an expense ratio may look like a small, one-time annual expense, your investment portfolio is actually hit with a double whammy. First, you’re charged the annual expense ratio on your current fund investment. Then, your lower returns are magnified by the smaller amount of money you have to compound over time.

Here’s how that might play out with two hypothetical funds:

You make an initial $1,000 investment in a fund with a 0.63% expense ratio, and then invest $6,000 a year for 30 years. The expense ratio would be equivalent to $6.30 per $1,000 invested. Assuming your fund earns an 8% average annual rate of return for 30 years:

- Before fees, your investment would be worth $744,137.86.

- After accounting for fees, it would be worth $659,029.93.

- The total expense ratio cost would be $85,107.93.

What if you choose a fund with a slightly lower expense ratio? With the same contributions and performance over time, a fund with an expense ratio of 0.31%, or $3.10 per $1,000 invested:

- Before fees, your investment would be worth $744,137.86.

- After accounting for fees, it would be worth $700,850.36.

- The total expense ratio cost would be $43,287.50.

YIKES! I feel like the most broken record on earth when I parrot, “Look for low fees, Polly. Look for low fees!” But this is why. It really and truly adds up over time. And, much like with MVNOs, you can get the same product for less. It is very, very, very worth the 15 minutes it’ll take you to google a fund and find its expense ratio.

If a fund is cagey about sharing their expense ratio? I’m willing to bet that’s because it’s higher than it should be. If a fund proudly displays their expense ratio? That’s probably because it’s nice and low. I would also like to point out that the example fund above, FSKAX has a lower expense ratio than Forbes’ example of a low-fee fund. Just saying.

And Fidelity is not the only brokerage to offer low-fee total market index funds: Vanguard’s VTSAX has an expense ratio of 0.04% and Charles Schwab’s SWPPX is 0.02%. If anyone has any other questions about expense ratios, please feel free to bring it up in the comments section and we’ll workshop it together.

Back To Eva’s Question

I hope everyone enjoyed that rather long sidenote about fund expense ratios. Let’s get back to the rest of Eva’s question on what to do with their $95k chunk of cash. As noted above, after designating some amount for their emergency fund, they could:

- Invest the remainder in the stock market:

- This would be the most aggressive approach with the highest potential for growth OR loss.

- In my opinion, the best primer on investing is the book, The Simple Path To Wealth by JL Collins, a version of which is in his blog’s “Stock Series” (affiliate link).

-

Salt Creek Falls Keep all of it in cash:

- This is the least aggressive approach with essentially zero potential for growth OR loss.

- Open a Roth IRA (Individual Retirement Account):

- A Roth IRA is a retirement account that’s post taxes.

- This means you pay taxes on the money you put into a Roth IRA, but you don’t pay taxes when you withdraw the money in retirement.

- A Roth IRA grows tax free.

- You must be age 59.5 before you can withdraw money penalty-free (although there are exceptions).

- Your eligibility to contribute to a Roth IRA depends on your income and your particular tax situation.

- I like this Nerd Wallet article on Roth IRAs if you want to read more.

- Open a Traditional IRA (Individual Retirement Account):

- A traditional IRA is a retirement account that’s pre-tax.

- This means you don’t pay taxes on money you put into an IRA, but you do pay taxes when you withdraw the money in retirement.

- There are no income limits. Anyone can contribute to a traditional IRA.

- You need to be age 59.5 before you can withdraw money penalty-free (although there are exceptions).

- More about traditional IRAs here.

- Do some combination of the above.

Eva and Patrick’s current retirement vehicles–their employer-sponsored 403bs–are pre-tax, which means you don’t pay taxes on the money you contribute to these accounts, but you will pay income taxes when you withdraw money in retirement. In light of that, if they wanted some tax diversity, a Roth IRA would offer them the opposite scenario: paying taxes now as opposed to later. We are verging into tax theory here, which is NOT my specialty, so I encourage Eva and Patrick to consult with an accountant about which tax strategy would make the most sense for them. The other thing to keep top of mind are…

Required Minimum Distributions

Also known as RMDs, these are amounts you are legally required to take out of various retirement vehicles once you hit certain ages. You’re not allowed to keep money in retirement accounts forever–at some point, the IRS requires you to start withdrawing money from them. In general, you have to start making withdrawals when you turn 72 (it used to be 70.5, but a law in 2019 bumped it up to 72). To be precise, “If you reach age 70 ½ in 2020 or later you must take your first RMD by April 1 of the year after you reach 72” (source). The exception are Roth IRAs, which you don’t have to take from until after the account owner is deceased.

According to the IRS:

The required minimum distribution for any year is the account balance as of the end of the immediately preceding calendar year divided by a distribution period from the IRS’s “Uniform Lifetime Table source: IRS.

What’s the “Uniform Lifetime Table”? I’m so glad you asked! The IRS provides it for us in this publication under the header, “Appendix B. Uniform Lifetime Table.” Per this table, the Distribution Period for age 72 is 25.6.

If Eva and Patrick begin RMDs when they’re legally required–at 72–the math they’ll do is the account balance of their 403bs and the account balance of their SEP IRA at the end of the 2036 calendar year (assuming they turn 72 in 2037), divided by the Distribution Period as listed in the above table.

Since we can’t know what those account balances will be at the end of 2036, let’s do the math using their current balances:

- Eva’s 403bs (all of them combined): $193,117 / 25.6 (the Distribution Period for age 72) = $7,543.63 per year

- Patrick’s 403b: $121,258 / 25.6 (the Distribution Period for age 72) = $4,736.64 per year

Since Eva has several old 403b accounts rolling around, the IRS notes:

…a 403(b) contract owner must calculate the RMD separately for each 403(b) contract that he or she owns, but can take the total amount from one or more of the 403(b) contracts (source).

Eva, you might want to roll all of these accounts together to simplify things.

Patrick has a SEP IRA, which is subject to the same RMD rules*, so he’ll do this math:

- SEP IRA: $1,020 / 25.6 (the Distribution Period for age 72) = $39.84

*I spent hours on the IRS website trying to definitively confirm that RMD rules for SEP IRAs are identical to those of 403bs and regular IRAs and…. I’m still not 100% certain. In some places on their website, the IRS makes it sound like SEP IRAs are governed by a different Distribution Period, but that period is not defined anywhere (trust me, I checked). Therefore, I decided to go with this:

The RMD for each year is calculated by dividing the IRA account balance as of December 31 of the prior year by the applicable distribution period or life expectancy. Use the Tables in Appendix B of Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs) (source).

If anyone has a SEP IRA from which they’re taking RMDs–or if anyone knows this definitely–and can confirm that the Distribution Period is the same, I will be VERY grateful.

The total amount they’ll be required to withdraw annually (using this year’s account balances) when they turn 72, is: $12,320.11.

The required amount increases each year, so they’ll be withdrawing more with each passing year. Be aware of that Uniform Lifetime table and the fact that the Distribution Period changes each and every year, correlated with your age.

Additionally if Patrick and Eva decide to open an IRA, that will also be subject to RMD rules; although a Roth IRA would not be (until after the death of the account owner).

Let’s Put It All Together Now

To recap, once Eva and Patrick begin taking Social Security and once they turn 72–the age when Required Minimum Distributions kick in–they’ll have a total annual income of $69,920.11. They can also choose to take out more than the RMDs if they’d like to have a larger budget. They can begin taking money from their 403bs penalty-free when they turn age 59.5.

These are estimates using today’s account balances and so Eva and Patrick will need to do the math at the time RMDs kick in for them. Laws change and the best way for them to stay on top of this is to read the IRS website. I prefer to use primary sources (such as the IRS and the Consumer Financial Protection Bureau) due to the changing nature of these laws. But, these estimates give Eva and Patrick a rough sense of the income they’ll have in retirement.

Here’s an abbreviated version of the above spreadsheet, now including their RMDs:

| Item | Amount (Annual) |

| Eva’s RMD from her 403bs (begins at age 72) | $7,543.63 |

| Patrick’s RMD from his 403b (begins at age 72) | $4,736.64 |

| Patrick’s RMD from his SEP IRA (begins at age 72) | $39.84 |

| Eva’s projected Social Security at age 67 | $26,604 |

| Patrick’s projected Social Security at age 65 | $30,996 |

| Total: | $69,920.11 |

| Year | Eva’s Net Income (Annual) | Patrick’s Net Income (Annual) | Expenses (Annual) | Net (income minus expenses) | Notes | Patrick & Eva’s Age (this is easy because they’re the same age!) |

| 2037 | $34,147.63 | $35,772.48 | $66,000 | $3,920.11 | This is the year that Required Minimum Distributions (RMDs) from their 403bs will kick in. | 72 |

More About Social Security

Let’s go back to the second part of Eva’s question on social security: If he doesn’t take SS benefits until 65, what happens during those three years? The benefit amount stays stagnant? Decreases from current estimates?

The amazing thing about Social Security is that it’s inflation-adjusted in perpetuity (source: Social Security Administration)! This is great news and it means your benefit amount won’t reduce. The other thing to know about Social Security is that the longer you wait before claiming your benefits, the bigger those benefits will be.

Eva discovered this in her research and it’s evident in the charts she included. You can figure out your anticipated Social Security benefits by following these instructions on how to retrieve your earnings tables from ssa.gov (the government Social Security website).

Patrick’s benefit amount will be larger the longer he waits to claim it, and, it’ll be larger than today’s estimates because it is inflation adjusted. I’m a primary source nerd, so I recommend the Social Security Administration website for further research.

Eva’s Question #4: Watching families at the hospital struggle with where to place a grandparent who has been living independently, and suddenly can no longer live independently, has me wondering if we should be looking into long-term care insurance now while we’re young enough to qualify for a lower premium? I originally thought we would do this when our term life insurance ended in 6/2027 (replace one bill with another).

I don’t really know the answer. It seems that a lot of longterm care plans don’t actually cover all that much. Plus, there’s no way of knowing whether or not you’ll ever use it. One option is to self-insure, which essentially means to save and invest money that could be used for longterm care if need be. The advantage of self-insuring is that the money isn’t tied up in an inaccessible account with restrictions on it. The disadvantage is that you might not save enough. If Eva and Patrick are interested in this, I suggest they research it and potentially speak with an insurance broker.

Eva’s Question #5: What, if anything, should we do with the SoFi account we opened?

I don’t see a SoFi account listed under assets. What type of account is it and how much money is in it?

Eva’s Question #7: How do we ensure the security of our personal information online? I really want to track spending, especially as a method for Patrick and I to realize our wasteful spending, but am very wary of using Personal Capital (or any software tool like this) because of the potential for hacking…all our account info in one location, YIKES!

The first thing to know is that your personal information isn’t secret to begin with and unless you do something grossly negligent, the chances of you being specifically targeted is miniscule. It’s much more likely a person will lose money by falling for a scam via email, text, or phone. Life is full of risks. Using online banking has risks as does walking across the street. For me, it’s a risk that’s well worth the convenience, much like using a credit card.

Here are some basics for staying safe on the internet, courtesy of my (now retired) software developer husband:

1) Always be a human firewall.

- Never, ever, ever reply to any email, phone call or text message asking for your personal information.

- Never turn your account numbers and passwords over to anyone else.

2) If someone calls (or texts or emails) you and says they’re from the IRS or your bank, etc, hang up.

- Do not give out personal information to such a caller, even if the phone number (or email address) appears to be legitimate.

3) After hanging up the phone, call your bank using the number on the back of your bank card to ask if there’s anything going on with your account.

4) Do not reply to requests for money or gift cards from anyone. Ever. If your cousin emails asking you to wire them money, don’t respond to the email. Call your cousin and ask them what’s going on. Chances are? Their email was hacked.

5) Do not click on weird links. Ever.

6) Have secure passwords and use a password manager. We use the password managing service 1Password and it is awesome (affiliate link).

I personally would worry much more about getting scammed than about having your information stolen from an online banking platform. In the event of a massive data breach, you’re in good company and it’s not you fighting to get your money back–it’s the corporation doing the legal work. Again, the biggest risk comes from you yourself voluntarily giving away your passwords, social security number, etc. That being said, don’t do anything you’re not comfortable with. I like and use the free expense tracking software from Personal Capital and for me, it’s worth the minimal risk, which is the same risk we encounter every time we open our computers and do things on the internet (affiliate link).

Other Stuff

A few final thoughts before we close:

1) High interest savings accounts: I suggest Eva and Patrick move their cash to a high-yield savings account. Interest rates are low across the board right now, but it’s still a good idea to move to a higher-interest account, even if it is a low percentage. One option that I like is the American Express high-yield savings account (affiliate link).

2) MVNOs: Eva is correct that they’ll save a ton of money if they switch to an MVNO. MVNOs (Mobile Virtual Network Operators) re-sell name brand cell service, so it’s the exact same service, just cheaper. It’s the TJ Maxx of the cell phone world! I use the MVNO Ting and I wrote this post detailing a bunch of different MVNO providers as well as a how-to guide (affiliate link).

3) Moving to a LCOL area: Eva mentioned a few times that they might want to move, but I’m left wondering why. They’ve paid off their house, they love their neighborhood and community, and their family and friends all live nearby. I know they’re concerned with the population growth of their town, but a larger town also offers more resources, which could be key as they age and particularly if Patrick’s family history of Alzheimer’s comes to bear. Perhaps moving will make sense for them from a financial standpoint, but I also think it’s important to love where you live–especially once you’re retired and spending more time at home and in your community.

4) Medicare: The monthly estimate Eva provided ($800) seems really high to me. I encourage them to spend time researching what their premiums are likely to be. And maybe $800 is correct, I just would want to back that up with research. Their retirement budget is fine either way, but gaining clarity on that huge line item will brings things into sharper focus.

Summary:

-

Forest walk Read the book The Simple Path To Wealth by JL Collins (affiliate link). Eva mentioned a few times that she feels uncertain when it comes to investing and this book is hands-down the best primer (in my opinion). JL Collins also writes the blog JL Collins and is close in age to Eva and Patrick, so he offers a valuable perspective that’s different from mine.

- I will also note that Eva, you know A LOT more about finance than you give yourself credit for!!! You and Patrick have done an AMAZING job managing your money over the years! Feel confident that you’ve got this.

- Consider rolling over Eva’s old 403b’s so that they’re all in one place. This will both simplify things from an administrative standpoint once RMDs kick in and will give Eva more control over what she’s invested in (remember to check those expense ratios).

- Tinker with the spreadsheet I made breaking down their retirement income and expenses by year. Everything appears to be on track for their planned retirement years and this spreadsheet should help guide their decisions should their income or expenses change.

- Be mindful of when RMDs kick in as you’re responsible for taking those withdrawals yourself.

- Check on the expense ratios for all of their investments to ensure they’re at a rate Eva and Patrick are comfortable with. Make adjustments as needed.

- Consider maxing out their 403bs for their remaining working years to provide extra retirement cushion.

- Decide what they want to do with their $95k in cash:

- Portion some out for their emergency fund. Move this to a high-yield savings account, such as this one from American Express (affiliate link).

- Determine if they want to invest the rest or keep it in cash.

- As noted above, investment options include (but are not limited to): taxable investments, an IRA, or a Roth IRA. Note the risks and tax implications of each choice.

- Research longterm care insurance to determine if it’s advisable.

- Consider paying for a password service, such as 1Password, to manage and keep secure all of their online passwords (affiliate link). Be aware that it’s much more likely/dangerous to be scammed by an individual than to fall victim to a data breached. Nothing is impossible and everything is a risk, but be aware of what’s statistically more likely to happen. Be a human firewall in all things!

- Also, your kids may be able to help you out with some of these tech things. Don’t be afraid to ask them for help! In many instances, it’s a question of setting something up once and then continuing to use it in perpetuity.

- Investigate transferring to an MVNO to start saving big buck$ every month.

- Contemplate why moving to a LCOL area feels important. It’s not strictly necessary from a financial standpoint because you’re on track for retirement AND your home is paid off.

- Feel really, really good about the excellent financial position you’re in. You’ve done an exemplary job and should feel confident and proud!

Ok Frugalwoods nation, what advice would you give to Eva? We’ll both reply to comments, so please feel free to ask questions!

Would you like your own case study to appear here on Frugalwoods? Email me (mrs@frugalwoods.com) your brief story and we’ll talk.

I have no financial advice to offer. I’m just here to say how sweet and adorable it is that Patrick colors her hair every three months.

THIS! love!

Thanks Jen! He’s been doing this for years. I should have kept track of the cost savings : )

Hi Eva and Liz! Lovely write up – I do find the case studies fascinating. I am wondering, since Eva’s kids will be in school for another few years, if it still makes and sense for them to start a 529 plan (before the end of the year!) and get the benefits of Oregon’s tax credit and some potential interest/returns. My kids are younger (10, 8, and 5) but the plan we use (different from our state, but our state doesn’t require use to use their plan for the tax benefit) has tiered levels based on age, so it’s a less aggressive investment depending on age (less risky). Just something to consider. I just scheduled my end of the year contributions for my kids and it was on my mind. Best of luck, Eva! I hope to be as prepared when I reach retirement age as you are.

Thank you for the great idea! I’ll look into a possible tax credit we might be able to take advantage of over the next year or two if we open a 529 even this late in the game.

Question #6 about Savings Bonds: If you don’t need the money, they continue to earn interest for 30 years after the purchase date. I’d keep them until you need them and use as mad money for a future purchase or fun item. Spreading out the cash-ins means less taxing on the interest.

Most are maturing at around the same time, but spreading them out as much as possible might help with the taxes. Thanks Debbie!

I’m not sure if this was figured into the Social Security estimates above, but when Social Security gives you an estimated amount for a certain age, they assume you will keep working at your current income until that age. So if you retire at 62 and do not take benefits until 70, your benefit at 70 will be less than if you had worked from 62 to 70.

The Social Security website has a calculator that allows you to enter any annual income for future years (rather than your current income) and will adjust estimates accordingly.

According to that calculator, in our case, if my husband stopped working at 62 and then collected benefits at 70, the monthly amount would be reduced by 20%, compared to working until age 70.

This is exactly what I was concerned about. It makes sense that it would be based on continuing to earn. And if the predicted reduction in SS comes to fruition, the two could equal a substantial reduction. I appreciate your input Belinda!

Just wanted to add clarification that social security is actually based on the highest 35 years salary. So if you have been working at the same inflation-adjusted salary from 25-60 you won’t get a reduction for fewer years, just based on what age you start claiming benefits. If you have lower earning years or time you took off for raising children, then you could end up with less than 35 full salary years, and continuing to work longer will increase your high-35 for social security. The SSA website assumes you will be working the next calendar year from when you check, but I haven’t seen anything that indicates it assumes you work another 10 years etc.

Yes! Thanks for clarifying that! I thought of that after writing my comment. In our case it makes a difference, but for someone who already has 35 years of solid income, they should be good.

Re. the website calculator, I think they assume you will work until you collect benefits and there is a box in which you can specify an average future income. It appears to me that they calculate with all future years at that figure. But once again, it won’t matter to folks who already have 35 good years paid in.

If you’re looking up your social security benefits (especially near retirement), you are much better off signing in to the SSA website and downloading a copy of your statements. This will give you a real prediction of what you will earn at different ages based on what you have paid in so far during your working life. Calculators on their website are not accurate and don’t take into account changes in work history and income throughout a potentially 40+ year working career. Hopefully the statements are where Eva is getting her numbers from! If not it is pretty easy to sign up for an account and download your information.

Mrs. Frugalwoods gives the great advice so mostly I just say “yeah, do what she says!”. So I guess I will give my own situation… I understand where you’re coming from completely. I’m not a rockstar nurse, but I’m on the other side of 40 with fledgeling adults thinking about my long term future. I’m also in the PNW and have watched our community grow 25% in the last 10 years. Our local independent coffee shop has become unbearably packed all the time and I think this fact alone warrants relocating out of state (I think I’m serious on that). For several years our plan was to stay in the state but move more rural like maybe south Sound or even the Islands (Oregon is great too but your state taxes income). The issue is that our older son is mildly autistic and he’s going to need more support than a typical young adult. We can’t just disappear some place hours away from society like, for example, the Olympic Peninsula. He has just recently picked electronics technologies as an associate’s degree and the program centers around biomedical applications so at least this opens up lots of options for future employment. For the last year we’ve been considering what our younger son might do. He’s the type that will go to a 4 year flagship university and maybe finish off with a graduate degree in something like law or business. But it could be anywhere and it’s dangerous for me to try and plan my retirement around his life. He loves California and his girlfriend loves Florida. Neither would work for us… instead I would give them enough cash to get an extra bedroom for grandma’s extended visits. 😉 The way we are different from you is that even though we have ten years here in the region, this has not become my home state. We don’t have the friends and family that you do. I would have a hard time giving that up, especially as I get older. In fact our plan is to move to the midwest where my parents’ families were from. Also, I sell one of our west coast homes and I can buy three in cash there, including a wonderfully restored Tudor for my husband and I. So despite the similarities in our situations the differences result in a different equation. If we had family here I would try to stay. We’d deal with the increase in population and COL. But as it is we are in a pretty good position to take advantage of geo arbitrage, especially since our older son has agreed to come with us. On the subject of investments… have you heard of Boogleheads? It’s an investment forum/philosophy that’s based on simplicity. There are people there that have 2 or 3 fund portfolios. Not entirely different than Mr. Money Mustache back in his day. In any case, I’m not a tech or investment person but I’ve found reading some of the information on that site helpful. I’m about to get an inheritance that goes beyond our savings and investment plans and I’m trying to figure out if I want to manage it myself or have Vanguard do it for me. It’s .3% which is pretty cheap, but in all honesty if it’s simply setting up index funds in an allocation and staying on top of it, well, I can probably do that myself. Decisions, decisions! Enough about me… if I were you I’d stay put. Not having a house payment, a nice pot of assets and friends and family means you’re set up pretty well. You’re in one of the most desirable areas in the entire country so if, for whatever reason, you do leave, depending on where you go you will reap the advantages of going from high COL to lower COL. You can think of it as an additional insurance policy for life.

I was concerned my husband wouldn’t be able to retire at 62 unless we took advantage of some of the equity in our home. Hence, we were thinking of LCOL locations. What you’ve mentioned about staying in an area where we already have friends and family is very true. I’m feeling less like we need to plan on moving after Mrs. Frugalwoods’ help : ). Thank you for sharing your insights!

Did you mean Bogleheads? I have heard of the Boglehead forum and their philosophy, but not Boogleheads.

We took a vacation out to central Oregon in 2019. The scenery in a few of your pictures look familiar! It’s absolutely breathtaking out there!

One thing I wonder is if you’re looking at getting a one-story house eventually, if you could just keep your eye on the market over the next few years. With all the capital you have in your house, I would think you’d be able to find a new house that will suit your future needs and still keep you in the area you love with your support network. Yes, the population increase is not ideal, but in my opinion, being close to a support network is worth so much.

I agree, and am feeling some relief after our case study that perhaps we can stay in our area, and like you mentioned, look for a single-story home here – YAY! Thanks Emily.

Have you considered retirement expenses and income after one spouse dies? The survivor will not continue to get both Social Security checks. Expenses may not go down a proportionate amount, especially if the survivor lives in the same house. Since one spouse could die decades before the other (in any couple), it’s worth checking the numbers for that scenario.

When I plan for retirement, I don’t even include my estimated Social Security benefit since either one of us on our own would receive my husband’s amount only. If we do both live to a ripe old age together (and Social Security continues to do its thing), we’ll have my checks as a cushion against surprises, but I don’t run numbers with it in mind.

A very good reminder! I’ll run Mrs. Frugalwoods’ scenarios without including my own SS benefit. Thank you.

There are social security survivor benefits that are paid to widows. You can get more information from the ssa site.

I would encourage you to start looking into Medicare now. It is a confusing system with penalties if you postpone applying for certain portions (part B & D) because you think you don’t need them. You will get a lot of pressure to sign up for a Medicare Advantage Plan, but please be aware that with your husbands family history, you may be denied traditional Medicare which he will need for the best coverage at a later date if you take the Medicare Advantage initially. This is a good FB group to get a better understanding of your options. https://www.facebook.com/groups/BoomerBenefits. Also, Liz is correct about Long Term Care Insurance. It is really not that good. I worked many years as a Patient Advocate (LTC Ombudsman) in Long Term Care facilities, so I have seen them all. It sounds like you have really done well in saving for your retirement and I don’t feel qualified to make other recommendations but wanted to give you a heads-up on the Medicare part.

Sally, I’m not arguing, I’m genuinely asking about being denied Medicare due to Patrick’s family history – I’ve never heard of that before. My husband had no issue getting Medicare, and his mother died of Alzheimer’s and he is a Type 1 (juvenile) diabetic. I was accepted without a problem and I have a pretty serious autoimmune condition. Can you expand on possible denial a little more, please ?

Thanks!

Sally, I was confused at first as well. Then I reread it. Someone will not be denied a supplemental policy when they first enroll in Medicare. However, if someone enrolls in an Advantage plan, and later (after the first year), wants to enroll in a supplemental plan, they might have to undergo medical underwriting and could be denied. They would still be able to go back to traditional A&B, but won’t necessarily have the option to purchase a supplemental plan, such as Plan G or N.

As a Nurse Case Manager, I agree with this. Stay away from Medicare Advantage Plans, even with their smooth advertising. Traditional Medicare will be a better choice when you need services, even if the costs are initially higher. You have to requalify for Traditional, health wise, if you leave it and it can be denied.

As a long term care nurse I agree don’t give up Medicare A even though Medicare advantage plans may offer dental you’ll get screwed if you need skilled nursing care. Long term care insurance is something that used to be great but insurers took a bath in the 90’s and don’t offer good coverage now.

We’ll definitely be applying for Medicare at 65 when I retire and no longer have employer-provided benefits. I’ll make a note of your information re: Medicare Advantage, and will also look at the FB group — thank you so much for the link!

Wow, interesting to hear all the thoughts on long-term care insurance! Sounds like saving move in a dedicated account, as suggested by Mrs. Frugalwoods, may be the route to go for this. I appreciate the insight.

Regarding help with retirement savings and investment ratios, both Fidelity and Vanguard associates are a great resource. Give them a call, and they will walk you through how to find any information, and ask them for suggestions for alternative investments. A free resource for being an account owner with them!

I would also add to long term care planning that speaking with an attorney specializing in elder law is a great idea. What is and is not allowed (such as creating trusts to shield assets from Medicaid clawback) are state-specific. However, these attorneys are a great resource for what is best in anyone’s personal and family situation. This has been immensely helpful for about $200 cost per hour with my aging in-laws in their 70s.

I just want to say you’ve done a great job saving for retirement and thinking things through, planning how much you’ll need, etc. I took care of my dad the last 4 years of his life. He had Alzheimer’s at least 15 years, and passed away at 84. He and mom traveled, moved an RV up to Colorado to stay in during summer, and traveled to Canada and parts of the USA after he retired at age 58. There is no guarantee who will or who won’t get dementia (I’m sure you know this) so I think you should enjoy life and plan on having to help take care of each other in old age whether either of you gets dementia or not. Families everywhere are grappling with how to take care of the folks. The best thing to do is be prepared to pay for in-home care which is less expensive and better quality than in a facility. Enjoy the last few years of working, and then enjoy retirement even more!

Yes, I care for many folks with Alzheimer’s at work. There are predisposing factors, but as you stated, you never know who will or won’t get it. Thank you for sharing your personal experience and the heart-felt advice Pauline!

You have a high income similar to what ours was; only my husband was working due to my ill health in the last few years before he retired. As an associate head of a large university library he brought home, the year before retirement in 2012, $5,938 net per month. I still gave occasional lectures for The National Association for the Humanities , which brought in maybe $350 more pr month.

We socked away ca $2,000 a month into a private annuity. I am older than my husband and took out social security when he retired as this raised my SS to a higher amount.

Now that we are both retired our current income is pretty much the same = $%5,971. , This breaks down to State of Delaware annuity i$2,600 a month. Private annuity $830 a month. SS 2131 a month SS 990 a month.

WE kept ready savings at between 10 and 25 thousand, for big expenses –new roof, new bathrooms, part new kitchen. ( Tile floors in all 3) All of which we have done since reTirement.

Medicare covers all doctor visits, all hospital stays with any surgeries. I have had heart stents, appendix removed, and hip replacement.

My husband has had 2 knee replacements and carpal tunnel surgery. All free. We do have additional Blue Cross Blue Shield insurance, paid by the university, and this pays most of our medical prescriptions ( We pay 20%) We are very lucky in this .

here is recent talk that Medicare may start covering eyes and teeth. Buy not yet. The University gives us some insurance for thes conditions–not good for eyes and better for dentistry. We pay nearly $60 off husband’s annuity for these. I have hd serious dental problems due to malnutrition as a child, ,in Eastern Europe. I go to a famous dental school at Temple University.. Philadelphia. Graduate students work on me with close supervision from the school’s professors, who sometimes take over. I have never had a higher charge from them more that $80 ( Partial dental plates) If where you move to `has a dental school this is the way to go.

Look out for State taxes before you consider moving elsewhere. Some States are very high. Although Delaware is expensive living–property especially, we pay no taxes as retirees. Every tax time we receive back $6,000+ which goes strait into savings.

This is a very long reply but I hope that you can pick out some useful ideas from it.

I wish you the very best, I really enjoyed your openness and life style–more so because we moved here, in 1992, from Corvallis, OR.

Erika W.

So funny, we were just in Corvallis TODAY, which is why I am so late in reading these very thoughtful comments. There is a dental school 3 hrs from us; I hadn’t even thought about it as a possibility for care. So much to think about surrounding retirement. I appreciate your input!

I’ve been thinking about dental insurance as well as I’ll be retiring next March at the age of 55. Another source of dental insurance is through AARP ($99/month for one person for comprehensive coverage in Massachusetts). I’m still working on the calculations about whether it’s worth it or not. I’m considering self-insurance instead and I love the idea of nearby dental schools – I’m going to looking into that.

Sorry, I meant I took out SS before he retired. Changed it to working of his SS when he retired ,because this raised mine.

You life sounds lovely – I really enjoyed reading about the many things in life that being you joy! I don’t want to be a major downer, but I do think you should consider the cost of long term care as your husband has dementia in his family tree. When we were trying to find a facility for an aging family member with early dementia, assisted living was punishingly expensive, and nursing home care was completely unaffordable. We were caught in a difficult position as he had too much income to qualify for aid, but nowhere near enough money to afford the care he needed. I think this is true for many middle class people, and it’s why so many families end up really struggling with providing in-home care for people who need 24 hour a day care and supervision. (I’ve also seen this, and it was incredibly hard for everyone.) It’s also why so many people end up on Medicaid – Medicare doesn’t cover long-term care, while Medicaid does. The problem is that to get Medicaid coverage, you have to first spend down all of your assets. Women obviously often live longer on average than men, and this is one reason why elderly women often struggle financially – the family has spent all of their assets on care for the first person to become ill. I’m not sure what the answer is here – I don’t know much about long-term care insurance, but my understanding is that it often doesn’t cover much. When my husband and I are getting nearer to retirement age, we plan on talking to either a lawyer or a fee-based financial planner with expertise in elder care so we can discuss the best way to be sure we’re both financially protected in old age. I was really horrified to realize how little support there is for middle class people who can’t afford long-term care. It is not something most people can reasonably save for (we certainly can’t – think potentially $100k per year for skilled nursing home care), so I would expect Medicaid to be part of the picture at some point if anyone develops dementia. The thing to look into is making sure that the surviving partner is financially protected. Hopefully this is never an issue, but dementia is so common that it’s worth exploring as part of planning for the future. I don’t think you should try to save for this – I just think you should talk to someone with expertise in elder care and financial planning to be sure you’re both financially protected.

Good advice. I have heard all the things you mention from the families of my patients and it is frightening. I also saw it firsthand with my father-in-law. Thankfully, he was able to stay home until he passed, but my mother-in-law could have used more help than we were able to provide. Thank you for sharing your insights!

First, let me say kudos on all the thought you have put into making the big step to retirement and your commitment to save $2K every month. I have a few comments to share that are based on personal experience. We retired in the last 2 years at 62 and 59.

* SS benefits continue to go up the longer you wait. If possible, one person should wait until they are at full retirement age to take SS benefits. That way even if that person dies first, the spouse can starting taking the higher amount.

* I am a strong believer in a large savings account that is readily accessible. So I would keep the $95K in saving. I know this is not the popular view, but I have a number of reasons for this. 1) You know you have this amount to fall back on. It isn’t going to go up or down with the stock market. Last year we found a bank offering 2.5% and moved a large amount of our savings to that bank. It only lasted for 12 months, but they are now paying .6% (still much more than any other bank) and we are still making money on our money. 2) If you retire before 65 you will need to pay your own health care. We don’t live in California so it may be different in Oregon, but Covered California (the system put in place for the ACA that is still in place) is based on what you earn, not what you have in the bank. So, we are able to live on our savings and only take a small amount out of retirement accounts (considered income for Covered CA), and get no cost health insurance and very low cost dental. The savings on health and dental insurance is likely more than we would make on an investment if we moved our savings to a investment fund. Plus there is no risk to our money, so we know it won’t go down. 3) We know that no matter what happens, we have available cash to cover it. If our car breaks down, we have the money to buy a new one. If we get stuck some place on vacation and have to spend a few extra days, we have enough money to cover it without stressing. 4) Having enough money to live for a few years is a huge piece of mind.

* Long Term Care decisions – in my experience with friend’s parents, LTC insurance does not pay for a lot of expenses and it only pays for 3 years total. Do your research, but you may decide it is a better financial decision to put the money in an account that you can use for LTC if needed.

* Motorcycles – It looks like you have different types of motorcycles that are used for different purposes. Is it possible to consolidate and only have one? This would save you money on monthly insurance as well as having money from selling off the other (or selling them all and buying one that your husband is happy with).

* Moving to an area with a lower cost of living – You may want to think about doing this when your husband retires instead of waiting until you retire. This would allow you to live more easily on one salary and invest the money you will have left over after selling your current house and buying a smaller one in a cheaper market. I am retired from administration at a large health care system and was privy to the hourly pay of RNs coming from other states so I know there is a huge difference in what an RN makes in different states and locations. You would want to make sure that your pay would not go down significantly if you move and what you would need to do to get licensed in the new state.

* National Park Pass – good news is when your husband turns 62, he can buy a life time pass for $80. So this will be a one time expense. The pass allows for 5 people to enter the parks. When we go with friends that don’t have a pass, they often offer to pay for lunch or buy us a drink because they benefited from our pass. So we get a double win!

Hi Nancy,

Would you please share the name of the bank that in now paying six percent interest on your emergency cash fund?

Thanks

Hi Heidi – I think she said 0.6% (a reduction from 2.5%), not 6%!

Poppy Bank. I believe they are paying higher for new customers for a limited time. They have a limited number of branches in Northern California.

This is a really good point on SS. It may work out much better to take Eva’s at 62 or 65 and then Patrick’s at 70. Then at 70 Eva can switch here to 50% of Patrick’s. It would make things a lot more financially stable in case one of the predecessors the other, and it wouldn’t have a large financial impact over those few years since their finances are in such good shape.

Regarding the very large emergency fund – what about investing some of it now and then building it back up when they are closer to 62 and want to build a buffer for the years between stopping work and collecting social security? Their work seems stable and their savings are high, so they don’t need to have the large cash cushion so far in advance in order to have one for retirement.

Agree with staying in your house/community. My parents have lived in one town since the 1970s. They have a huge social network – but now they are in their 80s and are considering moving to a retirement community to be closer to my brothers family. All change is difficult – but this is especially daunting.

It’s a blessing to be near family, in an area you like, and in a home that’s paid off.

If you think you might want to move, maybe consider buying some land. The price of real estate keeps increasing. Maybe it makes sense to purchase now rather than later (5-10 years) when it might be more expensive?

Medicare premiums for part B are based on income at 65. Most people pay around $150 per month, from what I can see. My own premium (I am still working) is $145 per month, and I hear some others say theirs is about the same. Once a person starts collecting SS, the premium is withheld out of the SS checks. Part A is free to most people, but does not cover much at all. Medicare part B will not cover everything, either, so also consider the cost of a supplemental policy. An agent can help you with this, but a lot of it is online as well. Part B doesn’t currently cover prescriptions, and has a yearly deductible as well as co-pays.

Also to be aware of – many health insurers use age-banded policies. Once a person is in his or her sixties, the premiums for a health policy, even one through work, can go through the roof. My monthly health premiums jumped to almost $1200 a month, while my younger co-workers’ were $350 – $550 a month. My employer paid a portion of it, but I had to pay the rest, until my employer decided to cover the entire premium for all employees’ health insurance. They now reimburse me for my Medicare premiums, which I pay myself.

Again, depending on total annual income, SS income is taxed on a percentage of the income, rather than the entire SS income, for most people. The IRS has a formula to figure that and tax software figures it for you when doing your taxes. This is just an FYI for thinking about your tax burden later.