Katie and her husband Jon live in Chicago, IL with their two-year-old daughter Amaia. But Chicago is not where their hearts are. Jon is originally from the Basque Country and the family longs to return. After a brief stint of living there in 2019, they were forced back to the States in order to find better jobs. Now, they’re on a three to five-year trajectory to retire early in Spain. They’ve asked for our help in analyzing their plan and forecasting the likelihood of this dream.

What’s a Reader Case Study?

Case Studies address financial and life dilemmas that readers of Frugalwoods send to me requesting advice. Then, we (that’d be me and YOU, dear reader) read through their situation and provide advice, encouragement, insight and feedback in the comments section.

For an example, check out the last case study. Case Studies are updated by participants (at the end of the post) several months after the Case is featured. Visit this page for links to all updated Case Studies.

The Goal Of Reader Case Studies

Reader Case Studies are intended to highlight a diverse range of financial situations, ages, ethnicities, geography, goals, careers, incomes, family composition and more!

The Case Study series began in 2016 and, to date, there’ve been 60 Case Studies. I’ve featured folks with annual incomes ranging from $17,160 to $200k+ and net worths ranging from -$317,596 to $2.9M+.

I’ve featured single, married, partnered, divorced, child-filled and child-free households. I’ve featured gay, straight and trans people. I’ve featured men, women and non-binary folks. I’ve had cat people and dog people. I’ve featured folks from the US, Australia, Canada, England, South Africa, Spain and France.

I’ve featured people with PhDs and people with high school diplomas. I’ve featured people in their early 20’s and people in their late 60’s. I’ve featured folks who live on farms and folks who live in New York City.

The goal is diversity and only YOU can help me achieve that by emailing me your story! If you haven’t seen your circumstances reflected in a Case Study, I encourage you to apply to be a Case Study participant by emailing mrs@frugalwoods.com.

Reader Case Study Guidelines

I probably don’t need to say the following because you folks are the kindest, most polite commenters on the internet, but please note that Frugalwoods is a judgement-free zone where we endeavor to help one another, not condemn. There’s no room for rudeness here–the goal is to create a supportive environment where we all acknowledge that we’re human, we’re flawed, but we choose to be here together, workshopping our money and our lives with positive, proactive suggestions and ideas.

A disclaimer that I am not a trained financial professional and I encourage people not to make serious financial decisions based solely on what one person on the internet advises. I encourage everyone to do their own research to determine the best course of action for their finances. I am not a financial advisor and I am not your financial advisor.

With that I’ll let Katie, today’s Case Study subject, take it from here!

Katie’s Story

Hi, Frugalwoods! I’m Katie, a 32- year-old American married to Jon, a 38-year-old Basque. Together we have a hilarious almost 2-year-old daughter named Amaia. We currently live in Chicago where I work in public relations and Jon works in logistics. We met on the OG dating site, Match.com back in 2011 :).

Jon had moved to Chicago for work and I was a recent college grad starting my career. We got married just 8 months after meeting to avoid having to do a long distance relationship when Jon’s visa ran out. 9.5 years and a daughter later, it was the best crazy decision of our lives!

Over the course of our relationship, we have lived in Chicago, Las Vegas, Spain and now we are back in Chicago. As a family, we love being outside – at the park, beach, in the mountains. And we love to cook – especially traditional Basque foods. Our dream is to retire early in the Basque Country and we’re hoping to do so in the next 3-5 years.

What feels most pressing right now? What brings you to submit a Case Study?

We’ve just moved from Spain to Chicago. We moved to Spain in October of 2019 with the intention of staying indefinitely. We planned for this move for nearly 5 years – saving diligently because we knew securing employment in Spain was going to be tricky. Spain still hasn’t really recovered from the 2008 recession and the job market is, well, shit. Luckily, I was able to keep my US job (and salary!) working as a remote freelancer.

Jon struggled to find work but finally received two job offers in February/March 2020 – one with a luxury tour company and another at a Michelin star restaurant. Then the pandemic hit, and both of his job opportunities disappeared. He spent the next several months applying for jobs with no luck. Finally, in October of 2020 (seven months later), he found a contracted position covering a medical leave. My employment has been fairly steady over the last year, I got furloughed for 2 months over the summer when things got really bad, but was brought back for some projects here and there and I’ve been back to full-time since October.

We knew Jon’s job contract would eventually come to an end and he had little hope of finding something new once it ended, so we started to think through our next move. We absolutely loved living in Spain, but we knew it would be very hard to reach our financial goals relying on employment options there. We started to play with the idea of moving back to the states for a few years, while our daughter is young, to finish out our financial goals. And JUST as we started to think about that, I got a LinkedIn message from a recruiter for a big job back in Chicago. After a series of interviews and some candid conversations with my current employer, I was offered a full-time, promoted position at my current company – I got the offer from the competitor and my company countered, so I decided to stay.

At the end of March 2021, we relocated our family back to the US with the plan to stay for about 3-5 years, hopefully returning to Spain before Amaia needs to start ‘real school.’ Our goal is to return to Spain with a fully paid off home + about $1M invested ($1,150,000 total NW) and based on our calculations/forecast, we think that could be doable.

The most pressing thing for us: what’s it going to take for us to feel comfortable and confident in pulling the plug on full-time employment?

Can we get it done in 3-5 years while living in Chicago? How can we try to enjoy the next 3-5 years in Chicago knowing we’ll be longing for our life back in Spain? Our move to Spain in October 2019 was premature but Jon was burnt out and needed to get home. We’d just become parents and needed help and support from family. The move was great but we both feel like we left something incomplete back in the states. Jon is kicking butt at his new job and is making a conscious effort to build community in Chicago but I do still worry he might get burnt out again, especially when winter returns. And I don’t want us to wish away the next 3-5 years – I want to enjoy life while we work toward our goals.

Additionally, we will both have access to Social Security in the future — we both will have reached the minimum years of work by the time we retire

Owning and Renting

We purchased a scary haunted condo in The Basque Country of Spain for $100k (we paid cash) in February 2021 and will be renovating it over the next 6-8 months. While we live in Chicago, we’re renting a one-bedroom apartment. We are pretty comfy in this one-bedroom and I see us living here for our entire time in Chicago. Plus, moving is the worst so we’re hoping to avoid that at all costs. We’ll live in the condo in Spain when we move back and envision that being our forever home.

We probably will not rent the condo out while we’re in Chicago. Jon’s sister might live there and cover costs (HOA, insurance, etc.) but if not, we’re thinking we will keep it empty to avoid the added stress of managing it from abroad. Since we paid cash for the condo, our only monthly carrying costs are the HOA fee and insurance.

What’s the best part of your current lifestyle/routine?

In the Basque Country, I love the pace of life and the focus on the outdoors. Our days off mostly consist of leisurely walks by the river, playing in one of the many parks and perhaps stopping by a bar or café for a drink and a pintxo. Quality of life in the Basque Country is very high – great weather, diverse geography, cheap and beautiful produce, universal healthcare, nearly free education. Life is focused on family and friends – not money or flashy things and that is extremely refreshing.

In the US, I have a wonderful network of life-giving family and friends. I’ve missed them all terribly over the last year and a half that we’ve been in Spain. I also really appreciate the ability to grow professionally – the job and side hustle opportunities in the US feel limitless.

What’s the worst part of your current lifestyle/routine?

In the Basque Country, the lack of job opportunities is really THE issue for us. The job market is tough – very few jobs are available for very low pay. It makes reaching our financial goals very difficult.

In the US, cost of living is the biggest barrier. Healthcare and education are the two biggest things – retiring early in the US feels like an impossible feat. In Chicago specifically, the weather is a real burden – we love to be outside, but in Chicago, we are indoors 6 months+ of the year because of the extreme weather.

Where Katie and Jon want to be in 10 years:

- Finances: We’d like to have successfully lived off 2-2.5% of our investments for 5-7 years

- Lifestyle: Living in the Basque Country of Spain, spending our days walking, working out, surfing, cooking, reading, napping, playing with our daughter, taking day trips to nearby towns, enjoying the mountains and beach and just generally living a slow-paced life. At this point, we envision Amaia being our one and only child.

- Career: Retired, perhaps picking up a few projects here and there if we want.

Katie and Jon’s Finances

Income

| Item | Amount | Notes |

| Katie’s net income | $7,433 | Katie’s net salary, minus the following deductions: health and dental insurance, 401k contributions, and taxes. |

| Jon’s net income | $3,725 | Jon’s net salary, minus the following deductions: health and dental insurance, 401k contributions, and taxes. |

| Parking space rental | $94 | We rent out our parking space in Spain, which covers our HOA costs for the condo |

| Monthly subtotal: | $11,252 | |

| Annual total: | $135,024 |

Assets

| Item | Amount | Notes | Name of bank/brokerage |

| Brokerage Account | $423,736.25 | This is our taxable investment account | Betterment; We are currently sitting at 82% stocks, 18% bonds, slowly moving to 70/30. Expenses are 0.25%. |

| Home Equity | $168,335 | We bought our Spain condo in cash for $100K and are putting about $70K into the renovation. We’re counting that all as home equity. | |

| Traditional IRA (Katie) | $100,443.32 | Betterment | |

| Checking Account | $21,317 | We’re using this money to pay taxes and for the condo renovations. The rest is our emergency fund. | Bank of America |

| Traditional IRA (Jon) | $17,094.38 | Betterment | |

| 401k (Katie) | $5,964.50 | ||

| 401k (Jon) | $300 | Just started contributing last week | |

| Total: | $737,190.45 |

Note: Katie’s dad plans to gift us $150K over the next 5 years – we received the first $30K increment in February of this year.

Debts: $0

Vehicles: none

Expenses

I added our current expenses in Chicago, but also wanted to share our average expenses in Spain to show what our early retirement life will cost.

Chicago |

Spain |

|||

| Item | Amount | Notes | Amount | Notes |

| Rent | $1,150 | Includes rent + heat/water | $50 | Since we own the house outright, we just pay HOA |

| Utilities | $25 | Just pay electricity | $154 | Water, gas, electricity |

| Daycare | $1,280 | Private daycare, full day, 5 days a week – includes lunch and snacks and diapers | $117 | Public pre-school, pay for food & diapers |

| Groceries | $500 | Includes food, house supplies, diapers, etc. | $400 | Includes food, house supplies, diapers, etc. |

| Cell phone | $o | Both of our jobs pay for our cell phones | $23 | Includes both of our cell phones |

| Internet | $74 | $66 | ||

| Home Insurance | $0 | We rent | $33 | |

| Car Insurance | $0 | Don’t have car in Chicago, use CTA | $43 | |

| Gas for the Car | $0 | Don’t have car in Chicago, use CTA | $60 | |

| Personal Care | $24 | 2 haircuts a year for Katie, 1 every 6 weeks for Jon | $19 | 2 haircuts a year for Katie, 1 every 6 weeks for Jon |

| Entertainment | $100 | 1-2 dinners out, a cupcake and a coffee here and there, drinks with friends | $60 | A pintxo or two each week, 1 menu del dia for lunch |

| Travel | $208 | 2-3 domestic trips, 1-2 international trips back to Spain | $250 | 1-2 international trips back to US |

| Gifts | $41 | Christmas, birthdays | $41 | Christmas, birthdays |

| Clothing | $50 | A few new things per year – a pair of shoes, a new coat, etc. | $50 | |

| Healthcare/Dental | $42 | Annual check-ups, co-pays, etc. | $11 | Just have to pay for dental |

| Chicago Monthly subtotal: | $3,494 | Spain Monthly subtotal: | $1,377 | |

| Chicago Annual total: | $41,928 | Spain Annual total: | $16,524 | |

Credit Card Strategy

We’re working on getting a credit card. We applied, but because we don’t have any open accounts in the US right now, we were denied 🙁 BUT we love the Chase cards and have gotten a companion pass on SW using promos. Big fan.

Katie’s Questions for You:

- Based on our financial situation, do you think it’s feasible for us to reach our financial goals by Summer 2024? Or should we plan to stay in Chicago an additional 1-2 years beyond that?

- What tips do you have for enjoying these years of working towards our goals?

- When we reach our goal, how do we muster the courage to quit our jobs and execute our plan?

- Logistically, how should we plan to live off our investments? We know about the 4% rule, but feel more comfortable using 2 or 2.5%. How do you set up the withdrawals from your investments?

- How should we factor in the currency exchange rate from USD to Euro? And the cost of transferring money from the US to Spain?

- Right now, all our money is in our US-based investment accounts + our condo/parking spot. Should we think about diversifying? Any tips? We thought about buying a rental property in Spain, however, we don’t have access to mortgages in Spain and so would need to pay everything in cash. Is this something we should consider?

- Any glaring places where we can optimize/reduce costs/etc.?

Liz Frugalwoods’ Recommendations

First off, massive congratulations to Katie and Jon for the stellar financial decisions they’ve made! Katie and Jon managed to stay out of debt, buy a home in cash and live well below their means. Through the combination of excellent salaries and frugal living, they’ve put themselves on the trajectory to retire early.

What shines through the most is their clear articulation of their shared longterm goals: they want to live a simple, outdoorsy life with their daughter in the location they love.

I point this out because at the end of the day, The Goal is not money. Money is the vehicle we use to reach The Goal. Well done to Katie and Jon for discerning the type of life they want to lead and for their willingness to work hard and sacrifice in order to make it happen. Ok, let’s get to it!

Katie’s Question #1: Based on our financial situation, do you think it’s feasible for us to reach our financial goals by Summer 2024? Or should we plan to stay in Chicago an additional 1-2 years beyond that?

This answer may surprise Katie and Jon, but I actually think they could retire much sooner than 2024. The catch is their stated desire of a 2 or 2.5% withdrawal rate. That is an incredibly low and conservative rate. I get the desire to be cautious, but there is such a thing a being too conservative.

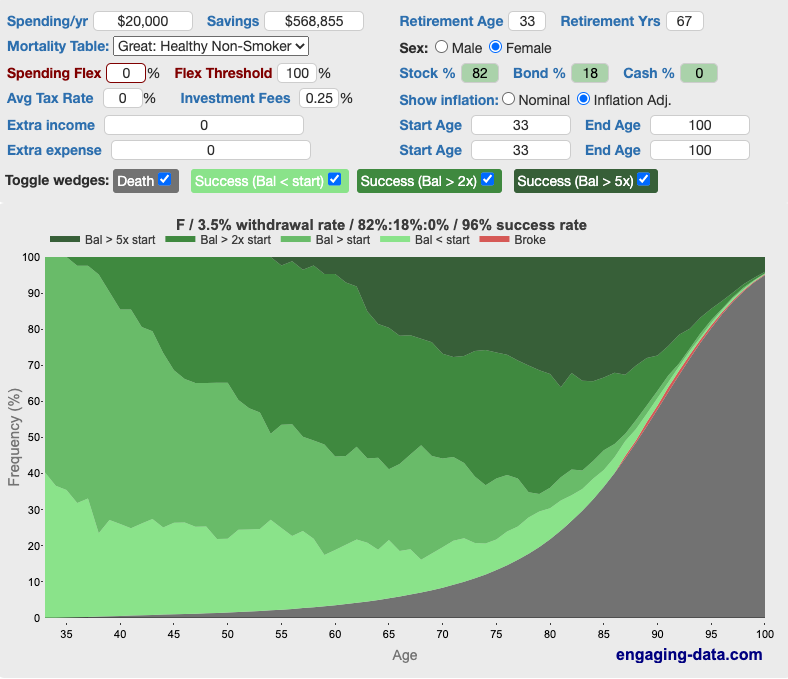

I am not an expert on withdrawal rates, but Early Retirement now is. I strongly suggest Katie and Jon read through his detailed, well-researched series of posts titled The Ultimate Guide to Safe Withdrawal Rates. I’m not going to paraphrase his entire series here, but I will include the below chart, which demonstrates the likelihood of running out of money at various withdrawal rates with various asset allocations:

Even assuming a long retirement–let’s say 60 years at an allocation of 75% stocks with a 3.5% withdrawal rate–you’ve got a 97% chance of your money lasting. And this doesn’t even count social security!! If you layer social security on top of a 3.5% withdrawal rate, you’re approaching a statistically 100% success rate, short of global cataclysm, in which case we all have much bigger problems than money.

The other graph I want to share is the “which will happen first: will I die or go broke?” Kinda morbid, but I think it’s an incredibly useful actuarial tool to help understand whether it’s more likely that you’ll die or go broke first:

As you can see, I input Katie and Jon’s details and, if they retired now and used a 3.5% withdrawal rate, there’s a 96% chance they’d succeed (in other words, they’d die before they went broke). Again, this is a good thing!

A few notes about this graph:

- This doesn’t include their social security payments, which Katie noted they’ll both be eligible for. That makes their success rate even higher!

- I increased their annual Spain spending from $16k to $20k as a buffer (more on that in a moment).

- This assumes neither of them ever makes another dollar after they retire (more on that in a moment).

- This keeps their asset allocation at 82% stocks and 18% bonds (more on that in a moment).

- You’ll note I used $568,855 as the amount saved because you can’t include home equity in these calculations. So $737,190.45 – $168,335 (home equity) = $568,855

I suggest Katie and Jon play around with this graph from Engaging Data.

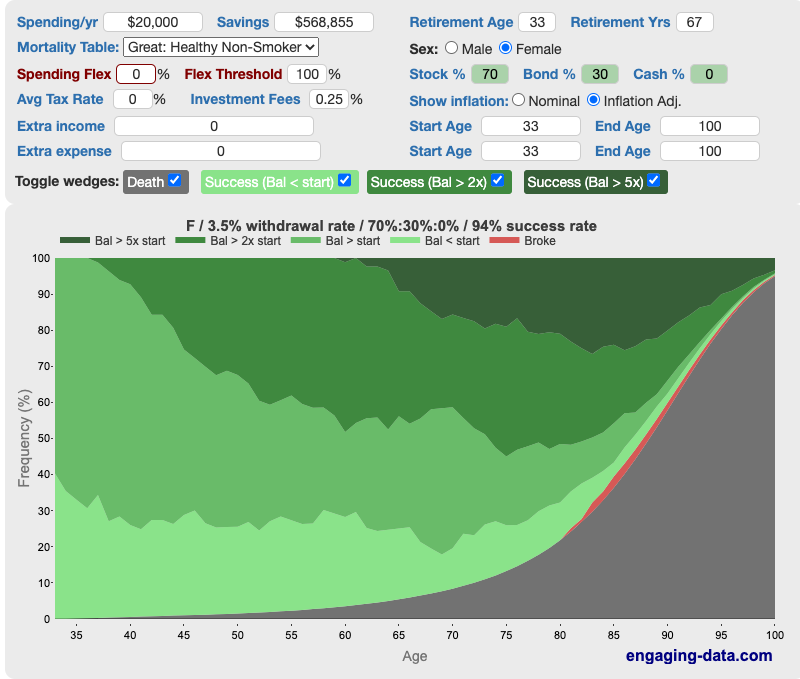

Asset Allocation

It’s rare that I tell people this, but, I think Katie and Jon are about to verge into the “too risk-averse” arena of investing. They are already at 18% bonds AND they have a paid-off house. Bonds are far less risky than stocks, but they’re also way, way, way less rewarding. They’re kinda like the turtles of investing–slow and steady, not much is going to happen, you’re in a shell so no one will eat you.

Stocks, on the other hand, such as a diversified total market low-fee index fund are sort of like the gazelles of investing–fast, exciting, but you could get eaten by a lion.

Risk is inherent to investing

You cannot invest without assuming risk. However, you also cannot expect to make money without taking risks. In my opinion–and it is opinion because I am NOT a financial professional–18% bonds (and a paid off house) at age 33 is already really, really conservative.

Katie’s note that they plan to go to 70% stocks and 30% bonds gives me the sweats. That is excessively conservative and carries a major risk of them missing out on market gains (see the last Case Study for detailed explanations of historical market returns).

But, in the words of Levar Burton, don’t take my word for it, check out what happens to the Retire or Die graph when I change the asset allocation to 70% stocks and 30% bonds:

Yikes on bikes! Things are still fine, but, their success rate decreases from 96% to 94% and you can see the red “broke” line creeping up larger in this allocation. I want to illustrate how important it is to pay attention to your asset allocation and I suggest Katie and Jon do more research and reconsider their desire to weight to 70/30.

Never Working Again?

Another angle I want to discuss is Katie and Jon’s assumption that neither of them will ever work again. That’s a really black and white definition of early retirement and, while that’s totally fine, it’s not the only option.

Personally and anecdotally, I don’t know anyone who is early retired and earns $0. Most of us–myself and my husband included–don’t work full-time and don’t have a salaried position. But many of us–myself and my husband included–do some stuff to earn some money every year.

The reason many of us do this is several-fold:

- We enjoy the work we do in early retirement. We do stuff we like and we do it part-time. I work maybe 15-20 hours a week (some week less, some weeks more), which is the perfect balance for me. I doubt I’ll ever go back to working more than that, but I also doubt I’ll ever work 0 hours because I love my job!

- If your expenses are low enough, you can cover them with your part-time early retirement work and not actually touch your investments. That is the beauty of frugality: the less you spend, the less you need to earn. Many of us aren’t adding to our investments with this part-time work, but that’s not the goal. We’ve already socked away sufficient investment portfolios, now they’re just growing in the market.

Katie and Jon’s Spain spending is wonderfully, amazingly low and I have to imagine Katie could earn that in a year with a few freelance marketing gigs. She noted she’s done freelance work in the past, which why I use her career as the example.

Doing this would eliminate (or reduce) their reliance on their withdrawal rate and would provide even more of a buffer for the long term. This isn’t a mandatory aspect for them–as we saw from the graphs above–but I think it merits consideration.

If I were Katie, I personally would rather retire now and freelance part-time as opposed to slogging away for another 3-5 years in a city I don’t like at a full-time job I don’t enjoy.

Other Spain Expenses?

Since a lot of this plan hinges on those low Spain expenses, I want to take a moment to do a gut check to make sure Katie and Jon aren’t missing anything.

Here are a few expenses I’m curious about:

- Capital expenditures and maintenance for the condo. Since they’re renovating, they may not have any major costs in the near future, but something is likely to come up at some point (roof, siding, oven, washing machine, random leak in the ceiling, child accidentally draws on wood floor with a magenta permanent marker… etc)

- They have “car insurance” and “gas for car” listed, but no line items for car purchase, maintenance, inspections, registration, etc.

- An accountant and/or tax attorney to manage ex-pat taxes and issues (more on that in a moment).

- And, a really big question: will the condo be big enough for the family in the longterm, when Amaia is older?

They may have already accounted for all these, but I wouldn’t be doing my (part-time, enjoyable) job if I didn’t bring them up. These are also why I rounded the $16k up to $20k for the above graphs.

Katie’s Questions #2 and #3: What tips do you have for enjoying these years of working towards our goals? When we reach our goal, how do we muster the courage to quit our jobs and execute our plan?

My response to both of these question is to do research. Research your plan, research your withdrawal rate, research your asset allocations, research freelance jobs, and research the fun things you’ll do once you move back to the Basque Country.

Research will do four things for Katie and Jon:

- Make them feel even more confident in their well-considered plans

- Hopefully encourage them to re-evaluate their withdrawal rate and asset allocation

- Help pass the time by focusing on their long-term goals

- Encourage them to perhaps pull the trigger and retire even sooner…

Katie’s Questions #4 and #5: Logistically, how should we plan to live off our investments? We know about the 4% rule, but feel more comfortable using 2 or 2.5%. How do you set up the withdrawals from your investments?

How should we factor in the currency exchange rate from USD to Euro? And the cost of transferring money from the US to Spain?

My answer is that I don’t know. I think they’ll probably need to hire an accountant/tax attorney specializing in US-Spain tax law since they’ll be filing taxes in both places. I would look for a Spain ex-pat forum where tax issues are discussed. I have to imagine there’s a robust online community that discusses these issues. Readers, please chime in here with your advice!!!!!!

Katie’s Question #6: Right now, all our money is in our US-based investment accounts + our condo/parking spot. Should we think about diversifying? Any tips?

We thought about buying a rental property in Spain, however, we don’t have access to mortgages in Spain and so would need to pay everything in cash. Is this something we should consider?

In general, the point of real estate investing is to leverage a mortgage. Paying cash usually isn’t the way to go if you want to make a return on the investment. This is another topic that I imagine comes up in these Spain ex-pat forums that I have to assume exist somewhere on the helpful frontier of cyber space.

In terms of keeping their investments US-based, this is just my opinion–but, in my opinion–I would keep my money in a US brokerage, in US dollars, and maintain a broadly diversified total market low-fee index fund of both domestic and international. That does mean you are subject to exchange rate fluctuations, which could be severe; however, the exchange rate risk is the price you pay for the stability of the US financial markets.

Katie’s Question #7: Any glaring places where we can optimize/reduce costs/etc.?

Nope! They are at Pro Level Frugal and, if anything, I’d be looking in the opposite direction: what expenses will need to be added in the future (per the discussion above). Also, if they don’t currently have renter’s insurance for their Chicago apartment, they should get it ASAP. It’s cheap and it’s important.

Summary:

Their investment horizon is very long and I’d think seriously about whether their asset allocation matches their longevity goals. Moving to 30% bonds seems prematurely conservative to me. It is fine to be conservative, but you have to balance risk versus longterm returns. Hopefully they’re alive for another 60+ years and 30% bonds in your 30’s is super duper conservative.

To that end, I suggest Katie and Jon:

- Read ERN’s The Ultimate Guide to Safe Withdrawal Rates series.

- Strongly consider varying their asset allocation (or leaving it at 82% stocks/18% bonds).

- Use the Retire or Die calculator to understand the likelihood of their plan’s success.

- Strongly consider increasing their safe withdrawal rate.

For example, a 3.5% withdrawal rate of their net worth (minus home equity) is $19,920 per year. At that rate, Spain is MORE than paid for right now. Then, at a historically safe withdrawal rate, they’re covered for the long term. If they work another year or two in Chicago, they can just continue to increase their savings and investments, but they’re mathematically ready to retire now.

Consider accelerating the timeline to move back to Spain and freelance part-time once there:

- Freelance in Spain for the next few years and see if their budget matches their projections.

- Let their investments grow.

- There’s really no pants-on-fire reason to be miserable for money right now, given their projections.

- Since their Spain expenses are so low, if Katie (or Jon) can freelance just a bit, it’ll make this a bulletproof plan since she might be able to completely cover their living expenses and not even touch their investments.

- She can always quit freelancing if she hates it and begin using a safe withdrawal rate. Conversely, she can ramp up freelancing if she really loves it!

For taxes and related issues:

- Find an online ex-pat forum.

- Hire an accountant/tax attorney who specialized in Spain-US tax issues.

Ok Frugalwoods nation, what advice would you give to Katie? We’ll both reply to comments, so please feel free to ask any clarifying questions!

Would you like your own case study to appear here on Frugalwoods? Email me (mrs@frugalwoods.com) your brief story and we’ll talk.

Thank you so much, Liz! We SO appreciate your insight. It’s so helpful to hear perspective from people who ‘get’ what we are trying to do. You’re not the first person to tell us we could pull the plug on full time employment now but potentially the most impactful. I would just say we are content for now — I don’t hate my job by any means and Jon is doing really well at his new job. I think we have at least a couple years of full time work let in us. 🙂

Good call on some of the expenses we left out – we WILL need to buy a new car when we get back to Spain. And by new I mean a 10+ year old car at about $7K max. Just something to get us to and from the beach/mountain. And keeping some extra funds for home and car maintenance will be important.

Will dive into the resources you shared — we have a lot of researching to do as we prep for the next stage including our allocation across stocks & bonds. It’s something we’ve gone back and forth on a lot so helpful to hear your perspective and see the charts. Something we will need to continue discussing.

You rock Liz!! Thank you so much for your hard work and amazing recommendations.

You really got me thinking about our assets allocation…we will probably change it to 80-20

Liz,

I would like to thank you for this amazing opportunity. While we had most of the answers or knowledge, we lacked that little push to make certain decisions. These are our updates since our story has been posted:

– We moved our investments to 80-20

– Set our return date to The Basque Country on August 2024. Our NW is estimated to be at about 1.1MM by then and Amaia will be right on time to start real school.

haircut estimate is far to low. We cut our own hair.

Guessing you mean too high. I did try to cut Jon’s hair for a brief period – it did NOT go well. Got any tips?

Haha. I feel you. I cut my husband’s hair during the pandemic and It did not go well either. I have a new appreciation for my hair stylist. Loved this case study as my husband I want to retire in Italy or France. Thank you!

The struggle is real, Karen! Italy or France sound like the perfect place to retire — southern Europe really know what they’re doing. Good luck you to!

You say that because you’re not familiar with Basque Country haircuts.

Katie’s little sister here! Extremely proud of and inspired by Katie and Jon’s impressive ability to put themselves in such an incredible position to retire early and live the life they dream of!

Thank you for sharing!

Love you, sister! <3

This is a case study after my own heart! My husband is also from Spain and we have a 1.5-year-old daughter, and we both have a yearning to move back as soon as the opportunity presents itself. You really, really can’t put a price on the quality of life in Spain- the culture, the food, the family connections, socialized health care, cheap public transportation, etc. I’m pretty envious of how close you are to that goal!

The one thing I would consider is if your expenses in Spain are truly reflective of living there versus just visiting. It sounds like you have done your homework and have thoroughly analyzed your spending habits. But my husband’s family is also very frugal (although not as pro as you), and I don’t think any of them could imagine living on $16,000 a year for a family of 3. When we did our own cost estimate when we were considering moving, we landed around 35-40k, and I think we had similar parameters as you did. We definitely don’t have a paid off house though, so we had rent considered in our expenses. But we estimated a couple coffees a week, 2 or 3 meals a month, low entertainment costs (although higher than your projection), etc. So you might try to go on a few expat websites and see if other families in similar situations would share their monthly budgets with you. And have your husband ask his family about your estimates too.

Another expense that seems low is your travel expense. We fly economy, using credit card points, on off-season dates, but for 3 people we still run around $2500 to $3000 per international trip. That is already about 250/month for 1 family trip a year with nothing else. If you think you might want to go twice a year, you’ll need to double that (unless you have a super-secret for cheap flights! Please share if you do!!). And you will be in Europe, so I suspect you might want to travel more “domestically” than you have in your budget. France is a couple hour drive away. Germany is a $60 RyanAir ticket, an airbnb in the south of Spain is a $100 a night. Even just camping, most dispersed camping isn’t allowed, so you’ll need to budget for campsites and driving. Just some other things to think about. 🙂

And lastly, and Mrs. Frugalwoods mentioned this, your daughter is still really young and if you are trying to plan long, long-term you may want to consider a separate line item for her expenses. They won’t be as low as they are now. For sure, they will be lower than in the States, but eventually, she might want to join a club sport or take an extra class, or go to the beach with her friends, etc. I know some families don’t pay for those types of costs or activities at all, but if you are trying to be thorough, it is something to consider.

Hi Rachel! Thanks for your thoughtful comment! Where is your husband from?? Crazy we have such similar backgrounds!

We got a taste of what living in Spain will cost us during our 1.5 year stint and while we were in pandemic times for a good chunk of our stay, I don’t foresee spending far beyond what we did. We averaged about $1,300 each month (not including housing – we lived with family). We will be living in a mid-sized town so not paying Madrid-like premiums for things like groceries or even drinks/dinners out. When a beer and a pintxo costs just $2, you can have a lot of fun for very little!

For travel – we have gotten extremely lucky over the last several years. The trick is to book your flight 6 months out. Our tickets have been about $400-600/per person, round trip on average. We use sites like JustFly.com to find the best rates. We will have all the flexibility so we can wait until the price is right before we book our flights. We are just 1 hour from the French border so I envision many close range road trips and a weekend trip here or there. Something we should definitely account for.

Good call on expenses for Amaia – so many activities in our town in Spain are FREE! The community center offers free music lessons, dance classes and lots more. Plus she will have access to the sports teams through school. BUT there will inevitably be things that come up that won’t be covered – so accounting for that in our future expenses will be important.

Thanks again for your input 🙂

If you haven’t done so yet, look into college costs for her. I’m sure it is WAY cheaper in Spain than in the US, but that will be a substantial expense that you may need to prepare for now rather than after you’re retired. I know it feels very far off when she is still young!

Hi Rachel,

Thank you so much for your comment! 35-40K in Spain seems extremely high to me…especially when a lot of “middle class” families don’t even make that as a net income a year.

Our year and a half back in The Basque Country was a great financial exercise for us. It allowed us to see and experience how our life can be there. We factored and averaged all the expenses we had during our time over there, including car improvements/repairs. surf boards, wet suits, surf classes and other kind of “one time” expenses. Some months were as low as 800E or as high as 1,500E (months where we bought surf boards, etc…)

In regards to international travels, we always scored great deals planning 6 months in advance. I guess we will even have more flexibility once retired.

Well, now you both have me second-guessing our projections! I tend to be very, very conservative when estimating expenses in general though. I always add a “miscellaneous” cost to every line item simply because my thought process is “I know I must be missing something, but I don’t know what” hahaha. Maybe my husband and I need to sit down again and see if our own move is more feasible than we expected 😉 He is from Madrid though, so I know that is going to be more expensive than other places though. Our rent estimate was 12K alone (1000 per month). I guess if we took that out, your estimate seems a lot more reasonable than I originally thought!

Your flights sound amazing- we’ve never snagged them that low, and we have even driven to Chicago to take a flight to Spain before. The lowest was maybe $750. I’ll check that website you recommended!

I also forgot that you both were there for over a year! So you definitely have a good idea of the budget you can expect. Now I’m back to just plain envious! Take us with you hahaha. Our daughters can become friends and practice Spanish and English and it will be so cute and beautiful. That is my literal dream!

Hi Rachel!

I know life in Madrid capital is much more expensive than in other parts of the country. However, you don’t really have to live in Madrid City if you are early retired. You could live in a more affordable nearby city like Toledo, Segovia or Avila…I bet you can have a higher than in Madrid for about 18-20K/year.

We just bought tickets round trip Chicago – Bilbao for January 2022 for $550/person with a great transit time. Again, Skyscanner was the cheapest option. I can’t stress this enough, but planning in advance and a little bit of flexibility has been key for us.

And Yes! some American friends in The Basque Country would be great 🙂

Hi. Katie and Jon seem to have a lot of convictions, and yet a lot of doubts, so I’m going offer some devil’s advocate thoughts (my background is that I’m a US expat, married to same, living in Ireland for 20 years). I wonder if the focus on Chicago and the Basque country is a little narrow, when you are entitled to live anywhere in the US and European Union. I get that you’ve already invested in your condo. And believe me, we were affected by the 2008 crash as well, we are familiar with the issues of unemployment/underemployment in the EU. But there has been recovery- it’s just not uniformly distributed, unfortunately. I understand Jon’s attachment to family and place, but unless that recovery extends through Spain, won’t Amaia have to relocate? (One of my own children has emigrated for work.) Also, it’s true of all relationships that an imbalance (in power, in opportunities, in needs being met) over time can be a strain. Living somewhere because you “have to” might be something that has to give (you seem to be experiencing in now in Chicago, but it could happen in Spain). Just keep in mind that you may feel differently about where to spend “forever” in twenty years’ time. I still deliberate. Right now, being able to get fresh corn on the cob in the States doesn’t outweigh the fact that US healthcare/insurance looks like it will never be (comparatively) affordable in my lifetime. But some days I still hope for a miracle. That’s how you can pass your time in Chicago, btw- enjoy your fresh corn on the cob (or whatever does it for you) or maybe a trip to the Everglades or Yellowstone while it’s easier. Now’s a good time to consult an accountant in each country too.

I had the same thought about what their daughter would have to do in the future, if prospects are still so slim there in the Basque country. That wouldn’t keep me from moving, but I might think about possibly helping to support her financially a while longer as she looks for good employment opportunities.

And I agree they could take advantage of the US’s diverse landscape and sights, and travel a bit while they are here, too. Winter might not feel so rough if you knew you had a vacation coming up in some place like Amelia Island (North Florida).

Cara and JD,

That is something we discussed. We do plan in helping our daughter financially and giving her guidance for the right education with more potential employment.

One of the reasons we are back in the US and want to save more money is because we would like to have the financial muscle to be able to help her out in many ways. We are also thinking in buying a condo for her and rent it out until she is ready to move in (like in 20 years or so :))

Same, same! I’m married to a Frenchman and live in a wealthy but relatively cheap area of France (though we are both by nature frugal, housing prices are absolutely bananacrackers!)

Please research what educational opportunities are available for your daughter. Right now, while she’s young, things appear and are probably fairly equivalent. Most places, rural, city, have good preschool and elementary. However, if your condo is located somewhere where she has to commute for 30 mins to an hour each way from school for middle and high school and lives far away from most of her future friends, that’s going to be a lot less doable in the future for her and for you! Take into consideration (my husband and I certainly have!) that you may want to move to a city when she’s in high school, which means higher COL.

You are probably looking into bilingual schools–if you’re not, you should be! If your area of the Basque country is similar to where I am in France, there are free bilingual programs in the public schools (Spanish-Basque in your case probably?). Make sure that wherever you live, you can keep going with the bilingual program. Ours goes all the way from pre-k to terminale (senior year of HS) and is completely public and free! What an incredible opportunity for her future and the future of the Basque language. However, for a guaranteed place, you must live in the area of town that’s districted for the program. Otherwise, you have to sign up for available places and hope for the best. This may alter your plans to live in the same condo indefinitely. But hopefully, since you’re both planners, you will have already considered this point 🙂

The travel costs seem waaaay too low to me for a couple of international flights. Maybe Amaia is sitting on laps right now, but that won’t last long. I don’t see saving for education expenses, bigger purchases (such as surfboards), nor home maintenance/improvements.

Congratulations on being in such a good place already!

@ Cara & Ariel

Jon here – We have been very meticulous with our travel plans. In the US we have been traveling for years basically for free because of our beloved Southwest Companion pass. We also had Airbnb credits because we used to rent a room out of our condo in Chicago, etc…

When we lived in Spain we traveled around a little bit. We stayed in Airnbnb, cooked in the apartment/house, etc… We also have access to a beach apartment close to The Basque Country where we are planning in spending long periods of time for free (my mother owns it)

As for international trips, we always plan our international trips 6 months out. I recommend skyscanner.com, always found great deals over there.

Thanks, Ariel! Appreciate your input!

We’ve gotten super lucky with cheap tickets but that luck could run out especially given current travel cost trends. Definitely something for us to keep in mind. Education is one of the big reasons we are planning to relocate – public education is mostly free and public university is very low cost – like $2-5K/year. A big game changer for early retirement.

Keep in mind: at the moment you are able to travel off season. If your daughter is in school, you must travel during the school holidays and prices go up. Flights during high seasons are often 1800 $ per person between Europe and the US (i always make reservations for a friend and know where to look for the best value for money)

Just spotted tickets Chicago-Bilbao in January for $570/person (470E) flying out on 12/31. I guess we will have the champagne on the plane. The key for us has been planning way in advance. In our case, we already know we are going in the winter and/or in the summer. Also, sometimes when it is a Holiday in the Basque Country is not a holiday in the US (which we use for our advantage). In this case, it is the three kings holiday which it is like a long extension of Christmas in Spain.

Why is renter’s insurance important? If you don’t have an apartment full of valuables why would you need it? Did you really carry it when you were renting?

My landlord requires it, in case you accidentally cause damage to the property. It also covers my belongings (which I would not have insured it it wasn’t included), and up to 5 days hotel if my apartment becomes uninhabitable (due to fire,etc). Just over $100 a year.

I’m addition to what Cindy said, it covers liability if someone gets hurt at your house and you are found legally responsible.

Renters insurance isn’t just for possessions it’s for personal liability. We know how litigious the USA is- if someone falls or is injured otherwise in your apartment, they may sue looking for the deepest pockets- the apartment owner and the residents. It’s a piece of mind thing. I’m surprised that their landlord doesn’t require it; the majority do. But here is a silver lining which I only found out about helping my (now departed) father with bookkeeping and billpaying . When he moved from a condo he owned to renting- going from homeowner’s to rental coverage reduces risk to the insurance company (they don’t have to rebuild the place after a fire, etc) , translating to a lower premium. HOWEVER, the biggest impact is that my dad gave up his license and I sold his car (all of this was not to his liking!). The majority of liability insurance cost is due to driving! So he ended up with insured possession of $20k, $2 million of liability coverage for $150/yr total! No I’m not missing a decimal point- basically no car/no (or little) risk! Most of us won’t know that because we still drive!

Renters insurance is extremely low (usually ~< $10/a month), especially for someone who has a child and therefore cannot as easily move out/couch surf in the case of urgent need to move out I highly recommend.

When our apartment became uninhabitable due to fire, completely moving out in a matter of days with a 3 month old was extremely stressful. However, it was much less stressful because renter's insurance covered full-service movers (who packed, moved and stored everything for us), and the different in rent on a temporary place while we searched for months for a suitable next place + most of our storage costs and the move into our next place.

Could we have done some of those things ourselves if we'd had to? Sure, but I'm glad we didn't

Wow congrats on all your hard work! In terms of enjoying your time left in Chicago, I might sit down and make a list of things you want to do in Chicago or even the US before you move, then make plans to do them. I know you’ll be back in the US to visit but it’s likely those trips will be dominated by family and friend time.

Thanks for the words of encouragement, CH! Great idea – there are definitely some places we had wished we visited before we made the first move to Spain – mainly national parks. It’s always nice to have things to look forward to.

Great situation to be in, Katie and Jon! And great analysis, Mrs. Frugalwoods.

I can understand the desire of Katie and Jon to provide a safe situation for themselves and their child. At some point you have to pull the trigger – which will always come with taking SOME risk – but I can understand why they don’t want to do that just now.

So I would suggest to find a nice compromise between retiring now (and being scared that your plans are going to fail) and scrimping and saving and retiring very very late (and missing out on years of happiness in the meantime).

Could you consider a timeline of 2 – 2.5 years to moving back to Spain? I use that timeframe because by that time your daughter might be ready for (pre)school and it could be good for her development in Spain to be in Spain by then. Use that time to build up your wealth some more, but also during that time use some of the money you earn to enhance the quality of your lives (like: fly to Spain a couple of times during those years).

Hopefully you can find that happy medium where the next couple of years are enjoyable, and your future is bright!

Good luck!

I think the closer we get to $1M invested, the easier it will be to condense our timeline. I see us reaching that milestone within the next 2-2.5 years. I also think if we get to a point where either of us is miserable, we will head back. It’s encouragement like this that helps us see we have technically already achieved our goal, anything we earn from now on is icing on the cake so to speak. Thanks for your encouragement, Petra!

This is really informative, and exciting to think they can retire earlier than planned. My only question is about the expense ratio of 0.25% on their brokerage account. That seems high, and could be a potential place for savings.

Hi Monica,

We currently use Betterment and has done wonders for us. I believe their expense ratio is one of the lowest in the market along with Vanguard. However, we are open to any suggestion!

Monica–thank you for bringing this up! Jon–for comparison, Fidelity’s Total Market Index Fund (FSKAX) has an expense ratio of 0.015% and Vanguard’s Total Market Index Fund (VTSAX) has an expense ratio of 0.04%. Both quite a bit lower than Betterment. Something to think about!

Thank you guys!!

I think I was referring to the robo investor tool that Vanguard offers.

How could we move everything to Vanguard without creating a massive taxable event?

If you don’t sell anything and move the money as a pure asset transfer between brokerages, it won’t be a taxable event. Not sure how this would work with a robo-adviser, but I’ve done this for other funds before. Importantly, you can’t switch funds without selling then buying again (which is taxable), but if the fund itself has a low ratio then you move it out of the robo-adviser and DIY.

Congratulations on such a well thought-out plan and your amazing diligence in reaching the investment level you’ve achieved! Obviously your financial discipline will lead to potential future years of happiness for your whole family.

You’re so young, though. Try to creatively think through some alternative scenarios from what you’re assuming of things that could change over the next 30 years. Any chance that your family size might increase? What if the health care scenario in Spain changes drastically? Suppose that your daughter wants specialized college training that would cost more than what appears now. Or a family medical crisis happens. (Not to be scary here, in any sense, but thinking ahead sharpens focus and planning.) Are you covered for such eventualities? We’ve learned that life happens, sometimes unexpectedly and sometimes expensively. I wish someone had told us, when we were young, to think ahead to the might-be’s. It would have helped us focus better on the long term.

As usual, Mrs. Frugalwoods has excellent suggestions. I wish you much happiness in the years ahead!

Are they sure they get free health care if they are not working in Spain and paid the social security taxes? https://www.expatnetwork.com/free-healthcare-move-spain/

Hi R Quinn! Jon and Amaia are both citizens so they have access automatically. I am a permanent resident with option to become a citizen in the near future. But even as a permanent resident, I had access to health care.

You might want to visit Yourthirdlife blog and see their experiences living in Spain and then returning to the US a couple of years later.

We will! Thanks, R Quinn!

R Quinn, I checked out Yourthirdlife blog, but it’s hard to get a full picture of their retirement. They seem to be freelance writers on other websites. Did they really return to the USA? Can you link to that piece of info? I’m curious why because they seemed to enjoy their life in Grenada in 2019-20.

This is a wonderful analysis. Really well done.

Good luck on the move!

Thanks Carey!!

Thanks Carey!

To make the next few years in Chicago more tolerable, perhaps look at ways to spend a little more to stave off burnout since that won’t derail your plans? Consider any destinations in the US you’d like to see that will become more complicated or costly to visit once your home base is in Spain that get you out of the Chicago winter. I’m in a location with extreme summer heat, and knowing I’ll escape to have even a weekend outside during the worst parts of the year gives me a short-term milestone that makes the tough days easier.

Good call, Jane! My parents are snowbirds in Arizona and we spent a few weeks with them right when we moved back. I could definitely see us escaping to visit them during the coldest months each winter.

Fellow European here, who have made the cross-continent move 3 times. I would recommend keeping your investments in the US, in US-based assets. If you sell all, when you move to Europe, you will face capital gains on any non-pension accounts. And you will not be able to transfer IRA’s or 401k pension accounts to Europe. The best way to transfer money is via Transferwise, and just go for selling the portion of your investments that you need to live on. Your annual income will be low enough to trigger no income tax (or minimal).

On the issue of taxes, as a US citizen, you need to file US taxes every year. Only federal, and no state, as long as you don’t have any earned income in any state in the US. If you freelance in the future and get paid in the US, then you will need to file in that state also where the employer is located. There is such a thing as ‘foreign earned income exclusion’, and also dual taxation treaties between most EU countries and the US. So, this means that you will file taxes in the US, but not owe any, because the tax rate you will pay in Spain is likely as high or higher. (Meaning, there is no taxation in the US, if you already paid taxes in the EU on the same income as a resident in the EU.)

Please research local taxation in Spain, as I don’t have any country-specific knowledge there.

Edith, I’m not sure this statement of yours is accurate: “On the issue of taxes, as a US citizen, you need to file US taxes every year. Only federal, and no state, as long as you don’t have any earned income in any state in the US.”

IMO (but I haven’t investigated), you first need to establish a residency in the no tax state (e.g.TX, FL, WY, and more) first before leaving the USA to avoid state tax filing. I think if you sell stocks/bonds, you still have to file a state tax return with the state you were a resident of before departure to pay cap gains tax….Or am I wrong? Thx

It varies from state to state, in my understanding – for example, I used to live in Vermont, and the information I got from the tax department there is that Vermont still considers you a resident for tax purposes until you establish residency in another US state (or Canadian province, maybe – I can’t quite remember) or if you are (or become) a citizen of a foreign country.

Thanks, Edith! Great to hear from someone who has made the move a few times. Great points all around – we did do some tax research for my freelance status – Spain doesn’t recognize freelancers, you have to set up a small business and pay a monthly small business fee in addition to the income taxes. If I freelance again, I’ll need to get that set up officially. We had started working with a local accountant just before we decided to move back. Something we will likely look into if I continue work when we return.

Go Curry Cracker has a lot of good information about the Foreign Earned Income Exclusion. He gets his taxes close to zero. https://www.gocurrycracker.com/

Foreign Tax Credit (FTC) may be more beneficial for them since they have a child (you are entitled to a cash payment for the child, which is currently $1400 per year) and since taxes in Spain are likely to be higher than in the US, which act as a credit against your worldwide income. Make sure you look into both before deciding to file FEIE.

Yes, and if you file under the Foreign tax credit you can carry forward or back excess foreign taxes paid and contribute to a Roth IRA. If you are in a higher tax jurisdiction it is much more beneficial.

Welcome to the expat life! I highly recommend TransferWise for moving money around. It’s consistently been the cheapest for us and will let you know if another company offers more competitive rates.

I also recommend researching how Spain taxes investments as it may change from the US.

Thanks Morgan!

Yes! Transferwise rocks!! we used to transfer money to buy our condo in The Basque Country and we saved about 4K in transfer fees.

I have no financial advice, just a deep jealousy of the connection to the Basque country. I love northern Spain so much (Catalonia has my heart) but last year right before pandemic my family visited the Basque Country and just adored it. I’ve honestly never seen so many happy and healthy-looking people (locals, out for their morning stroll along the waterfront, jogging, or chatting with friends with HUGE smiles on their faces). It’s clear that the lifestyle there is one that is a positive one, and I wish I could move there! Good luck, and thanks for sharing your pictures and your story!

It’s a pretty special place, so happy you had such a positive experience! Agree that people there seem so content with their simple but abundant life. Thanks for the encouragement 🙂

This post was exciting to see in my inbox this morning – I’m trying to convince my husband that we should move overseas to somewhere affordable and with a great lifestyle and weather, like Spain or Portugal (for at least a few years anyways). We have a young child about to start school, so navigating that will be trickier. We lived in London for a few years and loved all the places we travelled during that time.

I was thinking the same thing Mrs. Frugalwoods pointed out as I read this in regards to retiring completely at the time of the move. I may have misunderstood, but it sounded like Katie was fine with the freelancing work she was doing when they lived in Spain (i.e. didn’t hate her job, but maybe worked too much). Maybe they just didn’t have enough to support their lifestyle moving forward with that? I’d say if you like the work, and can do it on a part time and remote basis, you could continue to work for at least a few more years after the move and use that income to offset a portion of your expenses. This would allow you to move back to Spain sooner and/or beef up the budget for travel and some of the costs other commenters pointed out, but would still give you enough time to enjoy the lifestyle. Life is short and unpredictable, so if your current situation is going to make you miserable for the next few years, looking for a way to move up the timeline might be a better alternative.

Continuing part time work would also help to keep your withdrawal rate lower, which it sounds like you’re worried about. That might in turn make you more comfortable keeping the bond/stock ratio around 20/80 rather than going too conservative. Understandably, the historical stats aren’t always enough to help us sleep well at night so you’ll ultimately have to do what makes you comfortable so you aren’t retiring to a life of worry. Best of luck! I hope you’ll share more of your journey 🙂

great case study! I’m a Dutch expat living in the USA 🙂 love to see cross-national families and moves.

I also live in the midwest, in Madison, WI and my main tip for keeping the chicago time doable is to go outside more in winter. I bike and hike in winter, and as long as you have good gear it’s totally doable! I got most of my gear at the local thrift store’s annual outdoor brands event. Winters here are much colder but also much sunnier than my home country, and i actually love them a lot! Other things to try could be cross country skiiing, icefishing, etc.

Great points about winter recreation! We also get outside every day of the year–kids in tow–and it’s all about the gear and the mindset. I have a couple posts in case they’re helpful on this front: We’re Spending 1,000 Hours Outside in 2021 (maybe, we’ll see how it goes)

and

How We Recreate In Winter: The Gear, The Mindset, and The Baby Sled

Since I lean towards conservatism financially speaking, I wouldn’t jump the ship right now and retire back to Spain after returning from it recently. Katie’s salary is definitely awesome and if she likes her job, I’d suggest sticking at least for a year or two just to pad their savings/portfolio.

I know FW shared one chart from Karsten’s website, but for comparison, you should take a look at Pfau’s recalculated chart with his assumption that interest rates will stay low going forward. I cannot recall how I found it (I think while perusing articles on HackYourWealth blog) and it’s a tad different, not too terrible, but if you would like to see two points of view, it would be good to compare both charts.

Generally speaking, investing in the markets, the USA is the best and cheapest way. I don’t have experience with RE, so I wouldn’t know that.

I like such real life comparisons of living expenses in the US vs. other countries. You’ll be back to Spain in a short time. I think it’s just a matter of learning or tricking your mind to divert from the focus of “Spain is the best place to live and Chicago and its winters suck”. You’re both super young and full of energy. You can juggle one child and two well paid jobs for a couple of years for the 50-60 year security!

Anyway, my vote would be to tough it out ;-).

PS. Q.to Mrs.FW: Has your DH also ER’d now? I must have missed this little update.

P.S. Yes! I guess I should write a post about it :). HAH!

Hi Sail!!

Thank you very much for your kind words!

We are happy in Chicago at the moment. We just came back and are starting a new chapter (and somehow finishing the $$ accumulation chapter). We are very excited for the next couple of years and know what awaits for us…

I definitely need to do a better job than before at creating a good environment for myself in Chicago. However, I already made some friends, I like my current job and I feel quite optimistic about achieving our life goal.

This is a great case study! As a US citizen married to a South American this hits close to my heart. I completely understand the longing to move. It seems like y’all could go for it and succeed! I am curious about what Jon’s job is? Maybe he could be a stay at home dad and Katie continue to freelance/work. That could cut another expense once over in Basque country. I would recommend getting on Reddit, you can find lots of amazing subreddits where you can find people talking about things that interest you. A few of my favorites are /expats /povertyfinance /FIRE /leanFIRE there are so so many different forums and I’m sure you will be inspired! Good luck to you!

Awesome!

Thanks Quincy! appreciate the recommendations

Congratulations, Katie and Jon, for being so close to early retirement. I have just one suggestion not already made in the comments: if you haven’t already, consider reading the book The Aspirational Investor. It provided me with a framework to understand the different types of assets we hold, our allocation, and how each type of asset might perform in a severe market downturn. Although I had read a lot about asset allocation, I was never sure what was right for us. I used the information in the book to group our assets by category in a spreadsheet, and stress test them using market downturn scenarios from the book. It allowed me to be much more knowledgeable and confident about our plan.

Best wishes to you!

Hello Annie,

Thank you so much for the suggestion. Keeping that book for my to read list!

We are really questioning our assest allocation and thinking in moving it to 80-20% (Thanks FW for the encouragement!)

Another tool I used is the following:

https://portfoliocharts.com/portfolio/permanent-portfolio/

It has been designed by an Early Retirement Extreme member. Pretty informative and good visuals

Liz already shared the ERN chart on withdrawal rates but it’s worth repeating that a 2.0-2.5% withdrawal rate is very conservative. If you can become comfortable with a higher rate then you may be able to retire sooner than you think. The other thing to keep in mind with SWR’s is that they assume $0 income from any other sources. Life is both short and long at the same time and while you may have a young child now that you want to spend more time with, you could find yourself wanting to do some freelance or part time work later on which would require less income to be generated from your portfolio.

Overall, you’re in a good situation, good luck with your decision!

Thanks so much! Yeah I think this has given us a lot to think about – SWR, what the future of our employment might look like, if we could make a break for it sooner. Appreciate your input!

My husband and I flirted with the idea of moving to Italy a few years ago. There’s a group called International Living we followed.. We bought the book on Italy; it provided a lot of helpful information. I just checked their website. They have a free report on Spain (in exchange for an email address) and a $99 book on retiring to Spain. It might be worth checking out. The link is http://www.internationalizing.com.

Hi Renee,

First thing you want to investigate is how to be able to live in Europe legally long term (if you are not a resident already). Keep in mind that it is as hard as anyone who wants to move to the US. Some countries have programs for investors to be able to live and work. However, investments start at 500k and up.

Thank you for an interesting case! Really, my only recommendation is to work as long as needed to get social security. And enjoy your friends, family and visiting US places while being there. Good luck with everything!

P.S. Funny coincidence – I’m going to Chicago (from Atlanta) tomorrow with my best friend. Can’t wait to visit again beautiful architecture and to enjoy cooler weather 🙂

Thank you so much Olga!

Yes, I should be able to have access to SS after this year (since I would have worked 10 years in the US).

Enjoy your trip in Chicago! it is beautiful and hot!

we are a married American and German now with a family so I completely relate to your aspirations and conflicting opportunities being able to live in USA or EU! I am surprised no one has touched on how low your retirement accounts are in relationship to your brokerage accounts and income- the mad fientist has great blog posts about tax advantages of maxing out your yearly retirement contributions and how to use roth conversion ladder once you stop working to transfer money from Trad IRA to Roth IRA for further tax advantages and to access some of the money prior to hitting traditional retirement age but this gets tricky if you plan to live abroad. Go curry cracker is another great resource for dual citizen couples with emphasis on tax optimization (he’s American living abroad with his family). Thanks for sharing your financial world with us and also how to get cheap flights!!

Thank you so much for mentioning both Mad Fientist and Go Curry Cracker–both excellent resources!

Also Go Curry cracker explains how to do your own capital gains harvesting which is the only reason to use betterment and pay such high fees so certainly worth checking that out so you could manage your own brokerage investments directly with vanguard or fidelity as mentioned about and save a bunch in your Expense Ratio

LC,

Great input. We thought about managing our investments ourselves. However, we are not that knowledgable yet.

Also, if we would like to change everything to Vanguard at this point, we would have to basically sell everything and buy again with the brokerage account. Meaning, we would have to pay a good tax bill for capital gains, etc… Any advice on how to do this without (if possible) paying taxes or selling?

Jon, you want to do an in-kind transfer, which won’t result in a taxable event as long as Vanguard can hold the funds (and they take almost everything!) Here’s a good explainer: https://www.ajourneytofi.com/moving-a-taxable-account-from-betterment-to-vanguard/ These kinds of transfers typically need a medallion guarantee which is MUCH easier to get in the US than abroad. It takes a while and there are a bunch of hoops to jump through but it’s totally routine. Good luck!

Hi LC,

Yes, Katie is maxing out her 401K and I a taking full advantage of my 6% match.

I did have a retirement plan in the past that I had to cash out and invest it in our Betterment account.

The ladder conversion sounds interesting and we read about it before. However, we need to investigate more to fully understand it.

Big fan of Mad Fientist and Go Curry Cracker!

Hilary,

That is a great article explaining the process step by step. Love it!

Thanks!

May I suggest an emergency fund in Euros once you move to Spain? This will offset short-term currency fluctuations. Also, if you plan to invest any money in Europe, do consider a significantly lower withdrawal rate for this money (1-2%). Please consider that many European banks will not accept customers that pay taxes in the United States so while you will need a Spanish bank account it might be challenging to obtain.

Hello P,

Thank you so much for the suggestion! – Yes, part of our cash allocation is in a bank in the Basque Country. Our plan is having about 4 years of expenses in cash at all times, so we don’t really have to access to our investments in case there is a big crisis.

On another note, I have never heard of “European banks will not accept customers that pay taxes in the United States”. Their only request is either being a resident or a citizen of the country, Spain in this case. Katie had access to bank accounts as soon as she became a resident.

Some banks do not want the administrative burden of dealing with US citizens due to FATCA. She may have to fill out some additional paperwork if she changes banks . I got turned down at a number of banks in the UK, but it’s not impossible to find one. Being American abroad does come with some drawbacks,

In addition to qualifying for a local account based on residency, FATCA requires all banks worldwide to include a question along the lines of “Are you considered a US person for tax purposes?”

This isn’t based on whether the person thinks of themselves as American (or even if they’re a US citizen), or where they actually pay taxes. It’s *purely* based on whether the IRS considers this person a US person for tax purposes (which it does for all its citizens, as well as several other groups of people).

Customers who answer “yes” require far more KYC and ongoing regulatory headaches on the bank’s side, and there are banks that just can’t be bothered. You really shouldn’t have trouble finding a bank, but at the same time, there are some banks — often, either really small, local ones or extremely exclusive boutique ones that will politely decline.

Also, while Jon is a Spanish citizen, he’s presumably also a US citizen and should also answer “Yes” to that question (and comply with FATCA’s absurd rules for the rest of his life). Even if he’s not a US citizen, he should likely answer Yes, just to be safe.

The banks couldn’t care less, TBH, but because they’re on the hook if they do business with “US persons” without complying with FATCA, if they discover that anything disclosed to them was less than truthful, their only option is to be absolutely intransigent (think, frozen accounts, penalties, etc.)

Jay-nanas & Sam

Guys, banks out of the US world couldn’t care less where you are from as far as you are bringing money in and you are either a resident or a citizen (at least in Spain). I hold dual citizenship and never had a problem or have been asked, either had to fill up paperwork in regards to being a US citizen. The only thing we have to do apart from filling taxes, it is declaring our assets in each of the countries (1099G in Spain and FBAR in the US) Basically, the only purpose of it is avoiding money-laundering activities. Besides, the bank where we opened our account, it is an international bank and knows we are US citizens. Katie was able to have an account as soon as she became a resident.

I was coming here to say the same thing. Kids grow up and their clothing costs more, they eat more food, etc

Very true! Luckily we’ve got a pretty sweet hook up with some hand-me-downs for clothing. A very generous family friend who has 3 grand daughters. We haven’t had to buy many clothes so far – hoping that continues 🙂

In my experience, there is an avalanche of clothes that slows down about size 8 or so. We are down to one source of hand me downs for my ten year old and my twelve year old is 5’3 and wears a womens 2. Be prepared for everything to cost more as children get older. Our grocery budget has doubled in the past year and we have purchased three different wardrobes in the past year and three shoe sizes (soon to be four) because of the older girl’s growth spurts.

Even with being frugal, their costs go up as they grow. Our grocery and clothing budget probably doubled every three years or so until puberty- now it is skyrocketing with no end in sight😀

Rock those hand me downs, find your favorite thrift store, and Buy Nothing group. Sales and eBay are great for filling in the gaps.

Stephanie – I agree. I have 7 and 10 year olds and I am desperately trying to keep our grocery budget the same as it always was, but they keep eating more!

Re: clothing, I never had a consistent hand me down source, but I was always able to find cheap used clothing on Facebook marketplace, a bag of clothes for $5 type of thing. This worked great when the kids were small, and buying used still helps a lot, but now that they are older they are more picky about what they will wear, especially with pants. And shoes are expensive and hard to find used in good condition. And then there are always the one off things like they need black pants and a white shirt for the school concert and we have neither so we have to go out and buy.

I am also spending an exorbitant amount on extracurricular activities as my kids get older. Even stuff like music that is taught through the school so we don’t pay for lessons, we have to rent the instrument for $32/ month. All this stuff adds up.

Anyway, Mrs. FW added a little padding to Katie and Jon’s budget when doing her calcs so hopefully that will cover them if expenses surprise them as their child gets older.

Thanks Mrs. Frugalwoods for sharing the engaging data resource! I’ve been nerding out with it and it’s giving us a better idea of our options. What a great tool!

You are welcome! It’s a great one!

I congratulate the young couple on their excellent financial management and their ability to plan for the long term. My husband and I both retired at 60, though we both do freelance work on the side when we feel like it. I also am a life-long Chicagoan of a certain age (64!) and I have to take issue with the notion that you are basically home bound six months of the year! My husband do all kinds of things in every season — running, hiking, and walking even in the coldest weather. Chicago has so many year around resources — music, theater, sports, parks, museums, etc. And many events are free or affordable. We have a car but use public transportation or walk most of the time. My advice is to get out and embrace the cold! Chicago is a beautiful city 12 months of the year.

Oops. Meant to say My husband and I do all kinds of things … oh yes, add libraries to the list of resources! And the Old Town School of Music!

Hello Bea,

Yes, we (mostly me) need to change our mindset for the coming years, buy some good winter gear and get out no matter what. I am planning in joining a gym in the winter to able to continue running. I do want to get back to The Basque Country in top shape! 🙂

Such a fun case study, thanks for sharing! I second the advice to get outside all year round to make Chicago more bearable/fun. It’d start with a mindset shift (no bad weather, just bad clothing) and require some gear and perhaps a community. There are great all weather resources for getting kids outside (free forest school/get outside, Tinkergarten, nature play groups)

Thanks for the recommendations Hannah. We are also working on making some friends in similar situation like us – having small kids –

Here’s another “devil’s advocate” opinion – so take it or leave it: have another child. (I apologize if this is something that is not possible for you – just skip the rest of the post.) Have you heard of the “third culture kid” concept? Basically it’s a child that neither completely fits in the culture they’re living in but also doesn’t fit in the culture they’re from. TCKs are usually very adept at making quick friends and are often broader in their tolerance of others than their peers. But they can also struggle with not being able to form deep relationships or putting down roots. A sibling that is relatively close in age (a few years) can help TCKs navigate the culture mix because they’ll always have a sibling friend to share their “third culture” with. You plan to stay long term in Spain but plans can change and your daughter will still always be half American.